Insurance domain refers to the knowledge of how the insurance industry operates — its products, processes, regulations, and systems. For IT professionals and Business Analysts, insurance domain knowledge means understanding how insurance works as a business well enough to gather requirements, design solutions, write test cases, and deliver technology projects for insurance clients.

In This Article

What is Insurance?

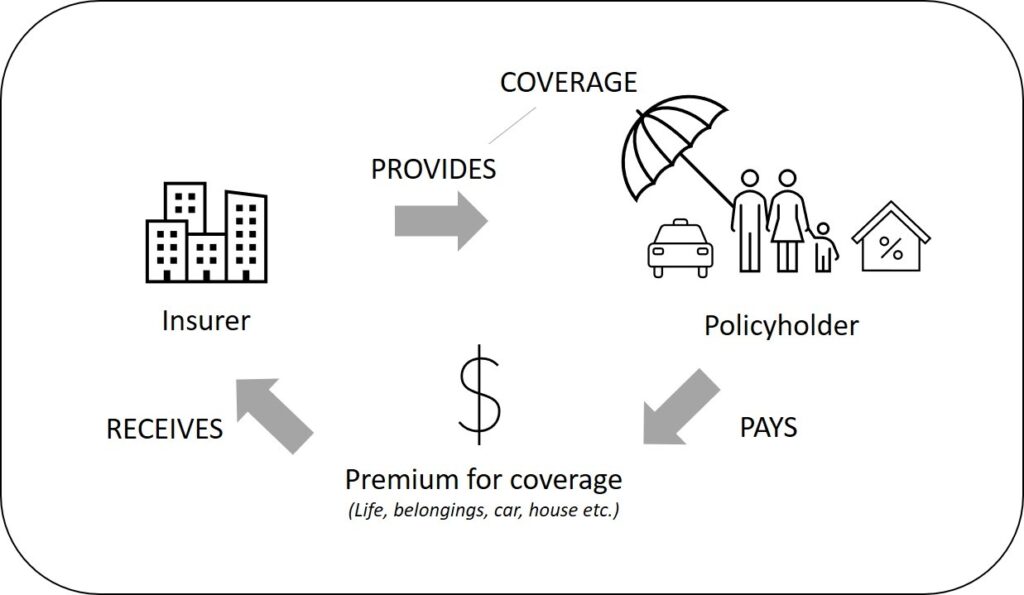

Insurance is a financial arrangement in which one party (the insured) transfers the risk of a potential financial loss to another party (the insurer) in exchange for a regular payment called a premium. In return, the insurer agrees to compensate the insured if the specified event — an accident, illness, death, or property damage — occurs.

At its foundation, insurance is a risk management tool. Individuals and businesses face countless uncertainties — illness, accidents, natural disasters, legal liability. Paying an affordable, predictable premium to avoid the risk of a large, unpredictable loss is the value proposition of every insurance product in existence.

For IT professionals and Business Analysts, understanding insurance at this conceptual level is the starting point. Everything that follows — the products, the processes, the regulations, and the systems — builds on this foundation.

How does Insurance work?

Insurance works on the principle of risk pooling. Many policyholders pay premiums into a common pool. At any given time, only a small proportion of those policyholders will experience a loss. The insurer uses the pooled premiums to pay the claims of those who do, while keeping the rest to cover operating costs and generate returns.

The chance that a loss event will occur is a statistical probability — actuaries calculate this probability based on historical data, which determines the premium rate charged. The higher the risk, the higher the premium.

The Insurance Business Cycle — End to End

| Stage | What Happens | IT / BA Relevance |

|---|---|---|

| 1. Product Design | Insurer defines coverage, exclusions, premiums for a product (e.g., term life policy) | Product configuration in Policy Admin Systems; rate tables, coverage rules |

| 2. Distribution / Sales | Policy sold through agents, brokers, bancassurance, or direct digital channels | CRM, agent portals, digital onboarding, e-KYC, bancassurance integrations |

| 3. Underwriting | Insurer assesses the applicant’s risk — decides whether to accept, modify, or decline | Underwriting workbench, risk scoring engines, third-party data integrations |

| 4. Policy Issuance | Accepted application becomes a policy — policy document generated, premium schedule set | Policy Administration System (PAS) — core insurance IT system |

| 5. Premium Collection | Policyholder pays premiums — monthly, quarterly, or annually | Premium billing systems, payment gateway integrations, lapse management |

| 6. Policy Servicing | Mid-term changes — address update, sum assured change, nomination change, revival | PAS endorsement workflows, self-service portals |

| 7. Claims | Insured event occurs — policyholder notifies insurer, submits documents, loss is assessed | Claims Management System (CMS) — FNOL, assessment, settlement workflows |

| 8. Settlement / Payout | Verified claim is paid — amount transferred to policyholder or beneficiary | Payment processing, fraud detection, reinsurance recovery |

| 9. Renewal / Lapse | Policy renewed at end of term — or lapses if premium not paid | Renewal workflows, lapse notice triggers, reinstatement processes |

In addition to collecting premiums and paying claims, insurers invest the premiums they receive to earn returns. They maintain claims reserves — funds set aside to pay future claims. Reinsurance (covered below) is also a key part of the picture, allowing insurers to transfer part of their risk to other insurers.

What Can Be Insured? — Principles of Insurability

Not everything can be insured. For a risk to be insurable, it must meet certain conditions:

- Pure risk only: Insurance covers pure risks — where the outcome is either loss or no loss. Speculative risks (like gambling or stock trading), where you can gain or lose, are not insurable.

- Definite and measurable: The event must be specific, the loss must be measurable in financial terms.

- Accidental: The loss must not be intentional — deliberate acts are excluded from coverage.

- Significant financial hardship: The potential loss must be large enough to cause genuine financial distress — trivial losses are not insured.

- Insurable interest: The insured must have a genuine financial stake in what is being insured. You cannot insure something you do not own or have no financial relationship with.

Insurance is formalised through an insurance policy — a legal contract specifying coverage, exclusions, premium, policy period, and conditions. For IT professionals building insurance systems, every field in a policy document corresponds to a data element in the Policy Administration System.

Types of Insurance

Insurance is broadly classified into three categories: Life Insurance, General Insurance (also called Non-Life Insurance), and Health Insurance. Insurance is one of the three pillars of the BFSI domain — alongside Banking and Financial Services.

Life Insurance

Key life insurance product types:

- Term Life Insurance — Pure death cover for a fixed period. Simplest, lowest premium, no maturity benefit.

- Whole Life Insurance — Coverage for the insured’s entire life. Builds cash value over time.

- Endowment Plans — Combination of insurance and savings — payout on death OR maturity.

- ULIPs (Unit Linked Insurance Plans) — Premium split between insurance cover and market-linked investment.

- Group Life Insurance — Single policy covering a group (employees, members) — common in employee benefits.

- Annuities — Regular income paid to policyholder, typically post-retirement.

For IT and BA Professionals: Life insurance IT projects commonly involve Policy Administration System (PAS) implementations, agent management portals, commission calculation engines, actuarial modelling tools, surrender value computation, and ULIP fund management integrations. Key processes to understand new business underwriting, policy revival, paid-up value calculation, nomination management, and maturity claim settlement.

Health Insurance

Health insurance covers the cost of medical treatment — hospitalisation, surgery, diagnostics, and in some cases outpatient and preventive care. In India, health insurance is regulated by IRDAI and sold by both standalone health insurers (like Star Health) and general insurance companies.

Key health insurance product types:

- Individual Health Plans — Covers a single individual for hospitalisation and medical expenses.

- Family Floater Plans — Single sum insured shared across family members.

- Group Health Insurance — Employer-sponsored coverage for employees — one of the largest health insurance segments.

- Critical Illness Plans — Lump sum payout on diagnosis of specified critical illnesses (cancer, heart attack, stroke).

- Government Health Schemes — Ayushman Bharat (India), Medicaid/Medicare (US) — large-scale public health insurance.

- Top-up / Super Top-up Plans — Additional coverage that kicks in after a deductible threshold.

For IT and BA Professionals: Health insurance IT projects involve claims management systems (cashless and reimbursement), hospital network management (TPA integrations), pre-authorisation workflows, health card issuance, portability processing, and fraud detection. Key terms to know: sum insured, deductible, co-payment, waiting period, pre-existing disease exclusion, cashless hospitalisation, and Third-Party Administrator (TPA).

General Insurance (Property & Casualty)

General insurance — also called non-life insurance or Property & Casualty (P&C) insurance — covers risks other than human life. It includes damage to property, vehicles, liability, travel, and commercial risks. Policies are typically annual and renewable.

Key general insurance product types:

- Motor Insurance — Covers vehicle damage (own damage) and third-party liability. Mandatory in India.

- Property / Home Insurance — Covers damage to buildings and contents from fire, flood, theft, etc.

- Commercial Insurance — Covers businesses against property damage, business interruption, liability.

- Marine Insurance — Covers cargo and vessels in transit — critical for trade finance.

- Liability Insurance — Professional indemnity, product liability, directors & officers (D&O) insurance.

- Travel Insurance — Covers trip cancellation, medical emergencies, baggage loss during travel.

- Crop / Agriculture Insurance — Government-backed schemes like PMFBY in India — large IT implementation projects.

For IT and BA Professionals: P&C insurance IT projects include motor claims processing, surveyor management systems, catastrophe modelling, loss assessment tools, FNOL (First Notice of Loss) portals, and telematics integration (for usage-based motor insurance). The P&C claims cycle is more complex than life insurance — involving field surveyors, salvage, subrogation, and reinsurance recovery. Key terms: FNOL, subrogation, salvage, loss ratio, combined ratio.

Reinsurance

Reinsurance is insurance for insurance companies. When an insurer accepts large risks, it may not have enough capital to pay all potential claims. To manage this, the insurer purchases coverage from a reinsurer, transferring part of its risk in exchange for a portion of the premium.

- Proportional Reinsurance — Insurer and reinsurer share premiums and losses in an agreed ratio.

- Non-Proportional (Excess of Loss) — Reinsurer only pays when claims exceed a defined threshold.

For IT and BA Professionals: Reinsurance processing is a key back-office function in large insurance companies. IT projects involve premium cession calculation, claims recovery, treaty management, and regulatory reporting. The reinsurance module in many Policy Administration Systems is complex and often requires specialised BA knowledge.

What is Insurance Domain Knowledge?

Insurance domain knowledge refers to a working understanding of how the insurance business operates — its products, processes, regulations, and technology systems — sufficient to perform an IT or Business Analysis role within an insurance environment.

It is not about becoming an actuary or an underwriter. It is about knowing enough to speak the language of insurance stakeholders, understand their business problems, and translate those problems into technology solutions.

Key Areas of Insurance Domain Knowledge

| Domain Knowledge Area | What It Covers | Why IT/BA Professionals Need It |

|---|---|---|

| Insurance Products | Term life, health plans, motor insurance, property coverage — how each product is structured | To understand the data model of a Policy Administration System and requirement context |

| Insurance Processes | Underwriting, policy issuance, premium collection, claims, renewals | End-to-end process understanding is essential for requirement elicitation and test case design |

| Regulations and Compliance | IRDAI (India), PRA/FCA (UK), NAIC (US), Solvency II, IFRS 17 | Regulatory requirements drive a large percentage of insurance IT projects |

| Insurance Systems | PAS, CMS, Agent Management, TPA portals, reinsurance systems | Knowing which system does what prevents scope confusion and incorrect system design |

| Insurance Terminology | Premium, sum assured, underwriting, deductible, co-pay, FNOL, subrogation, cession | Using correct terminology builds credibility with business stakeholders immediately |

| Insurance Data | Policy data, claims data, actuarial data, agent data, premium accounting | Data analysis and reporting projects require knowledge of what the data represents |

Insurance Domain for Business Analysts

Business Analysts working in insurance have one of the most complex domain environments in IT. Insurance contracts are legally binding, regulatory requirements are constant, and the data models are intricate. Domain knowledge is not optional for a BA in insurance — it is the job.

| BA Activity | Without Insurance Domain Knowledge | With Insurance Domain Knowledge |

|---|---|---|

| Requirements elicitation | Does not know which questions to ask; misses critical business rules (waiting periods, exclusions, rider structures) | Asks the right questions; understands the full policy lifecycle from the business’s perspective |

| Writing user stories / BRDs | Stories are technically vague; misses edge cases (lapse and revival, partial withdrawal, paid-up) | Writes complete stories with domain-accurate acceptance criteria and edge case coverage |

| Stakeholder communication | Constantly stops to ask for clarification on basic insurance terms | Speaks the language of underwriters, claims officers, and actuarial teams fluently |

| Test case writing | Generic test cases miss insurance-specific scenarios | Writes test cases for premium calculation, sum assured changes, maturity computation, claim settlement |

| Gap analysis | Cannot identify gaps between business requirement and system capability | Identifies gaps in existing PAS functionality vs new regulatory requirement |

Key Insurance Projects BAs Work On:

- Policy Administration System (PAS) implementation or upgrade — the most common large-scale insurance IT project

- Claims Management System implementation — life claims, health claims, motor claims, property claims

- Digital distribution platform — online policy purchase, e-KYC, agent portal, bancassurance

- Regulatory compliance projects — IRDAI filing changes, Solvency II, IFRS 17, AML/KYC

- Analytics and reporting — loss ratio dashboards, claims trend analysis, premium leakage detection

- Legacy modernisation — migrating old mainframe PAS to modern cloud-based systems

Insurance Domain in the IT Industry — Systems and Projects

The insurance industry is one of the largest consumers of IT services globally. In India, insurance IT services represent a significant portion of BFSI IT work — with major insurers like LIC, HDFC Life, ICICI Lombard, and Star Health running large-scale technology transformation programmes.

| Insurance IT System | What It Does | Common Project Types |

|---|---|---|

| Policy Administration System (PAS) | Core insurance platform — manages the entire policy lifecycle from quote to maturity/claim | New PAS implementation, PAS upgrade, product configuration, migration |

| Claims Management System (CMS) | Manages the claims process — FNOL, investigation, assessment, settlement, recovery | CMS implementation, claims portal, fraud detection module, surveyor management |

| Agent / Broker Management System | Manages the distribution network — agent onboarding, licensing, commission, performance | Agent portal, commission calculation engine, distribution analytics |

| Customer Portal / Self-Service | Policyholder-facing digital platform — policy view, premium payment, claims submission | Digital onboarding, self-service portal, mobile app for insurance |

| TPA Integration (Health) | Third Party Administrator manages cashless claims network with hospitals | TPA portal, hospital network management, pre-auth workflows |

| Reinsurance System | Manages risk cession, treaty management, recoveries from reinsurers | Reinsurance module, bordereaux reporting, recovery processing |

| Regulatory Reporting | Generates statutory reports for IRDAI, MCA, RBI (for bancassurance) | IRDAI filing automation, Solvency II reporting, IFRS 17 implementation |

| Analytics / BI Platform | Loss ratio analysis, claims trending, underwriting profitability, fraud scoring | Data warehouse, BI dashboards, predictive modelling for claims fraud |

Core Insurance Concepts and Principles

The following concepts form the foundation of insurance domain knowledge. For IT and BA professionals, understanding what each term means at a business level is essential for insurance project work.

| Term | What It Means | Where IT & BA Professionals Encounter It |

|---|---|---|

| Premium | The amount paid by the policyholder to the insurer at regular intervals — monthly, quarterly, or annually — in exchange for insurance coverage. | Premium billing module in PAS; grace period logic; lapse triggers; premium accounting; direct debit and payment gateway integrations |

| Sum Assured / Sum Insured | The guaranteed amount the insurer will pay on a valid claim or at policy maturity. Called “Sum Assured” in life insurance and “Sum Insured” in general insurance. | Core data field in every Policy Administration System; drives maturity benefit calculation, tax certificate generation, and claim assessment |

| Policy | The legal contract between the insurer and the policyholder. Specifies the coverage, exclusions, premium, policy term, and conditions under which claims will be paid. | Policy data model in PAS; policy document generation; endorsement workflows; every field in a policy document is a data element in the system |

| Underwriting | The process of assessing the risk of an applicant and deciding whether to accept the risk, at what premium, and with what conditions or exclusions. | Underwriting workbench in PAS; risk scoring rules engine; medical report and third-party data integrations; automated vs manual underwriting workflows |

| Claims | The formal request made by a policyholder to the insurer for financial compensation after an insured event — death, accident, hospitalisation, property damage — occurs. | Claims Management System (CMS); First Notice of Loss (FNOL) portal; document management; claim assessment workflow; payment processing and settlement |

| Rider / Add-on | An optional benefit attached to a base policy for an additional premium. Common examples include critical illness rider, accidental death benefit rider, and waiver of premium rider. | Product configuration in PAS; rider premium calculation logic; claims eligibility rules — a claim on a rider requires separate validation from the base policy claim |

| Deductible / Excess | The amount the policyholder must pay out of pocket before the insurer pays the remaining claim. Common in health and general insurance. Also called co-payment in health insurance. | Co-payment calculation logic in health Claims Management System; excess deduction in motor claims settlement; deductible rules are a frequent source of disputes that BAs must map carefully |

| Exclusion | A specific event, condition, or circumstance that is explicitly not covered by the policy. Common exclusions include pre-existing diseases, self-inflicted injury, and acts of war. | Claims rejection rules engine in CMS — one of the most complex components to configure; exclusion logic must be mapped precisely during requirements, as incorrect exclusion rules lead to wrongful claim rejections |

| Surrender Value | The amount paid to a policyholder who exits a life insurance policy before its maturity date. Calculated based on premiums paid, policy duration, and the type of policy. | One of the most complex financial calculations in life insurance IT; surrender value computation module in PAS; involves guaranteed surrender value (GSV) and special surrender value (SSV) — both must be configured correctly |

| Reinsurance / Cession | The arrangement by which an insurer transfers a portion of its accepted risk to another insurer (the reinsurer) in exchange for a share of the premium. The transfer is called cession. | Reinsurance treaty module in PAS; cession calculation — what proportion of each policy’s premium and risk is passed to the reinsurer; bordereaux reporting; reinsurance recovery processing when a claim is paid |

| Actuary | A professional who uses statistical and mathematical methods to calculate insurance premiums, reserves, and risk models. Actuaries determine the price of every insurance product. | Actuarial models feed directly into PAS for premium rate tables and reserve computation; BAs working on pricing or reserving projects need to understand actuarial data inputs and outputs even if they do not build the models |

| Loss Ratio | The ratio of claims paid to premiums earned, expressed as a percentage. A loss ratio of 70% means the insurer paid out 70 paise in claims for every rupee collected in premium. | Core KPI in every insurance analytics and BI project; loss ratio dashboards are among the most common reporting deliverables for BAs in insurance; a high loss ratio signals underwriting or fraud problems |

How to Build Insurance Domain Knowledge

Building insurance domain knowledge as an IT or BA professional is different from studying for an insurance exam. You do not need to become an underwriter or actuary. You need enough knowledge to be effective in insurance IT projects. Here is a practical path:

Step 1 — Learn the Insurance Business Lifecycle

Understand the end-to-end process from product design through to claims settlement. The Insurance Business Cycle table in Section 2 is a good starting framework. Know what happens at each stage and which system handles it.

Step 2 — Know the Key Insurance Products in Your Market

If you work with Indian insurance clients, understand the IRDAI regulatory environment, LIC products, standalone health insurers, and motor insurance. If you work with US/UK clients, learn the relevant P&C framework, Medicare/Medicaid, or Lloyd’s market structure.

Step 3 — Learn Insurance Terminology

The glossary table in Section 8 covers the core terms. Go deeper on the terms most relevant to your current project — a claims project needs deep claims terminology, a PAS implementation needs deep policy lifecycle knowledge.

Step 4 — Understand the Key IT Systems

Know what a PAS does vs a CMS vs a TPA portal. Even without hands-on system experience, knowing the functional scope of each system type prevents scope confusion on projects.

Step 5 — Get Structured Domain Training

Self-study is useful but takes time and often misses the practical, project-relevant context. Structured insurance domain training designed for IT professionals accelerates the learning curve significantly.

Techcanvass offers a dedicated Insurance Domain Course for Business Analysts, Testers, and IT professionals. The course covers the complete insurance lifecycle, product types, key IT systems, and domain-specific BA and QA scenarios — everything you need to hit the ground running on an insurance project.

Frequently Asked Questions

What is insurance domain?

What is insurance domain knowledge?

What does a Business Analyst do in the insurance domain?

What is a PAS in insurance?

What are the types of insurance?

Conclusion

Insurance domain knowledge is a career essential for any IT professional or Business Analyst working with insurance clients. The insurance industry — spanning life, health, general, and reinsurance — is one of the most technology-intensive and regulatory-driven sectors in the world. Understanding how insurance works as a business is what enables IT professionals to deliver projects that meet the business’s needs.

The foundation is the same regardless of which insurance sub-sector you work in understand the product, understand the end-to-end process, know the key systems, learn the terminology, and stay current with the regulatory landscape. Build this knowledge deliberately and systematically — and you will find yourself in demand for insurance IT projects at every level.