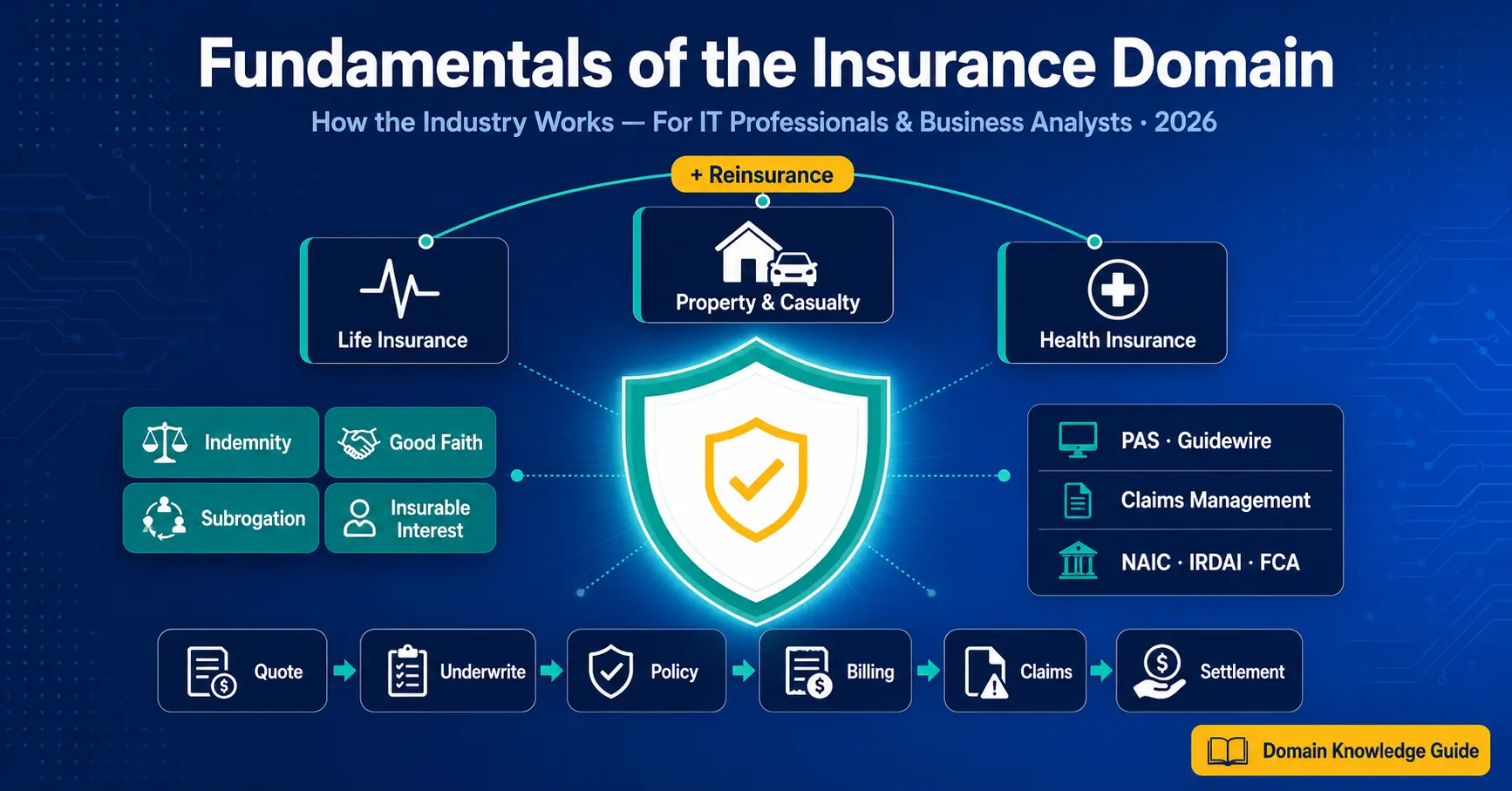

Fundamentals of the Insurance Domain: How the Industry Works

A practical guide to how insurance works, covering core principles, primary product categories, the insurance lifecycle, key terminology, IT systems, and what IT professionals and Business Analysts need to know worldwide.

What is the insurance domain?

The insurance domain is the industry sector encompassing all organisations that provide financial protection against risk: life insurers, general (property and casualty) insurers, health insurers, reinsurers, brokers, and their regulators.

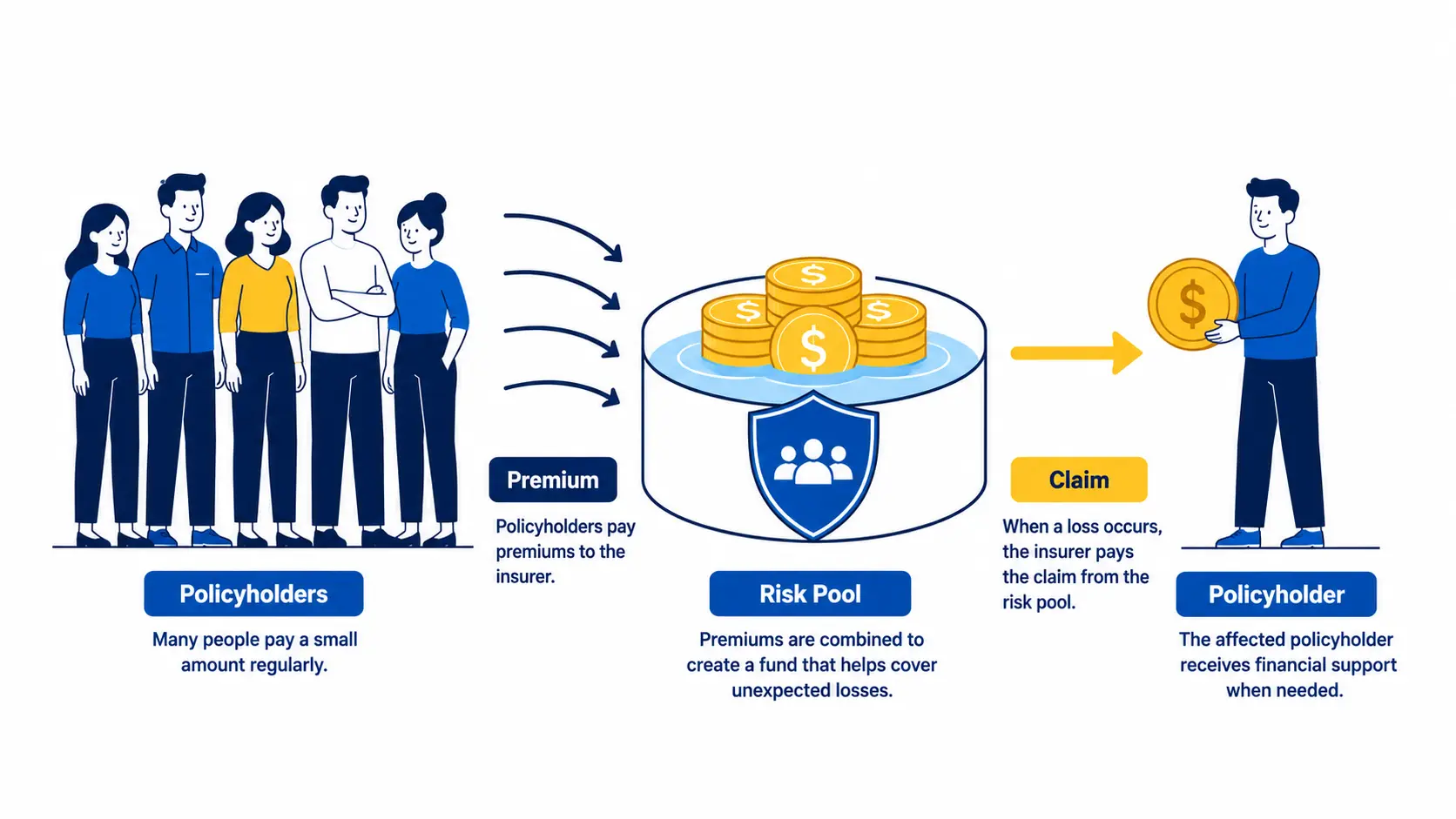

Insurance works on a simple principle: one party (the insured) transfers the risk of a financial loss to another party (the insurer) in exchange for a regular payment called a premium. The insurer compensates the insured if a specified event occurs.

For IT professionals and Business Analysts, the insurance sector is one of the most data-intensive and regulation-driven verticals in technology, making domain knowledge a high-value, in-demand skill globally.

What this guide covers

- 1Core principles: indemnity, insurable interest, good faith

- 2Product categories: life, health, P&C, reinsurance

- 3The insurance lifecycle: underwriting to claims

- 4IT systems: PAS, Guidewire, Duck Creek, Majesco

- 5Regulations: IRDAI, PRA/FCA, NAIC, Solvency II, IFRS 17

What Is the Insurance Sector?

At its core, insurance is a financial arrangement that replaces uncertainty with certainty. Rather than face the risk of a large, unpredictable loss alone, individuals and businesses pay a small, predictable premium to an insurer who pools those payments and compensates whoever experiences a covered loss. The insurer prices each policy using actuarial science, applying statistical probability to determine the likelihood and cost of future claims.

Insurance is one of the three pillars of the BFSI domain (Banking, Financial Services, and Insurance). It is a multi-trillion dollar global sector: the US alone accounts for over $2 trillion in annual premium volume, and the global insurance market exceeds $6 trillion. Major players include Allianz, AXA, Ping An, Berkshire Hathaway, Chubb, and Zurich in general insurance; MetLife, Prudential, and Sun Life in life; and Cigna, UnitedHealth, and Bupa in health.

Global insurance premiums

Annual premium volume across all insurance lines worldwide (Swiss Re, 2024).

Global insurtech investment

Cumulative technology investment in insurance since 2012, accelerating with AI and cloud transformation.

Life, Health, and P&C

The three primary product categories, with reinsurance as a risk-management layer across all three.

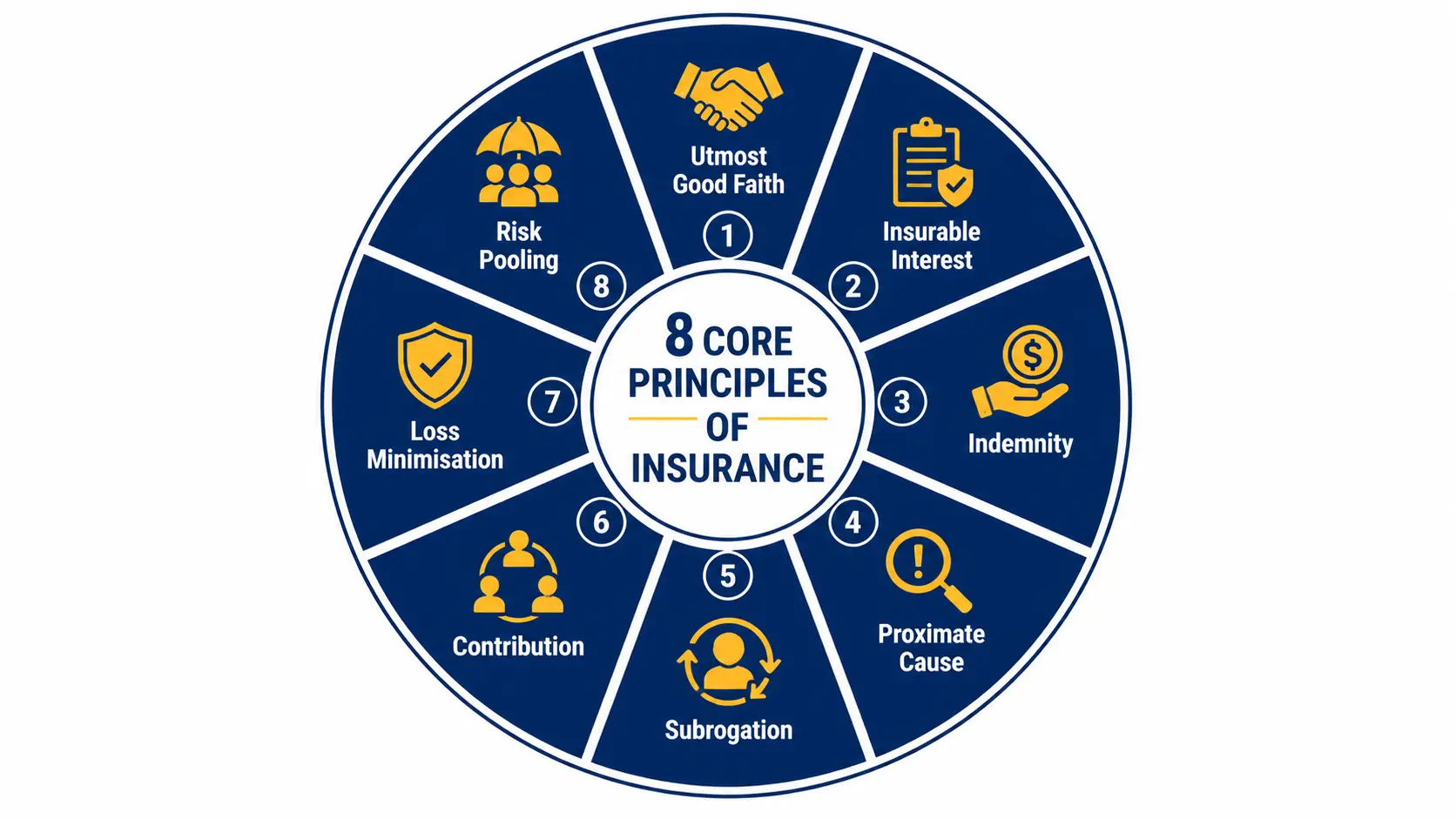

Core Principles of Insurance

Insurance contracts are governed by a set of foundational legal and ethical principles. Every insurance policy, regardless of country, product type, or insurer, operates within these rules. Understanding them is the first step to understanding how insurance actually works.

Utmost Good Faith (Uberrimae Fidei)

Both the insurer and the insured must disclose all material facts honestly and completely. Concealing relevant information can void the contract. This is the foundation of every insurance relationship.

Insurable Interest

The policyholder must have a genuine financial stake in what is being insured. You can insure your own home or vehicle, but not your neighbour’s. Without insurable interest, the contract is not enforceable.

Indemnity

Insurance exists to restore the insured to their exact financial position before the loss, no better and no worse. You cannot profit from an insurance claim. This prevents insurance from becoming a speculative tool.

Proximate Cause

A claim is only valid if the direct, uninterrupted cause of the loss is a covered peril specified in the policy. If an excluded event set the chain of events in motion, the claim may be denied.

Subrogation

After paying a claim, the insurer inherits the insured’s right to pursue recovery from any responsible third party. For example, if a third party caused a fire, the insurer can sue them after compensating the policyholder.

Contribution

If a risk is insured under more than one policy, all insurers share the cost proportionally. No insured can recover more than the actual loss across all policies combined.

Loss Minimisation

The insured must take all reasonable steps to minimise a loss, as if they were uninsured. Deliberately allowing a loss to grow, or failing to act, can reduce or void the claim.

Risk Pooling

Many policyholders pay premiums into a common pool; at any time only a small proportion experience a loss. The insurer uses pooled premiums to pay claims, while actuaries set rates using historical loss data.

Why this matters for IT and BA professionals: These principles are not just theory. They drive concrete system requirements. Indemnity affects how claim settlement amounts are calculated. Subrogation creates recovery workflows in claims systems. Insurable interest determines onboarding validation logic. Every principle has a corresponding process and system feature.

Primary Insurance Categories

The insurance industry is broadly divided into three product categories. Each operates differently in terms of risk type, policy duration, claims handling, and the IT systems that support it.

Life Insurance and Annuities

Life insurance provides financial protection against the risk of premature death, or in savings-oriented products, a guaranteed payout at maturity. Annuities provide a guaranteed income stream, typically used for post-retirement planning.

Term Life

Pure death cover for a fixed period. Lowest premium, no maturity benefit. Most common in US and UK markets.

Whole Life and Endowment

Lifelong cover, or insurance plus savings that pays on death or at maturity. Common in Asia-Pacific and India.

ULIPs and Variable Life

Premium split between life cover and market-linked investment funds. Requires investment and insurance system integration.

Group Life and Annuities

Single policy covering employees or a group; annuities provide regular post-retirement income streams.

Property and Casualty (P&C) / General Insurance

General insurance, called Property and Casualty (P&C) in North America and Non-Life in other markets, covers risks other than human life: property, vehicles, liability, marine, and commercial risks. Policies are typically annual and renewable.

Motor / Auto Insurance

Own-damage and third-party liability. Mandatory in most jurisdictions. Largest P&C line by volume globally.

Property and Homeowners

Damage to buildings and contents from fire, flood, theft, and natural catastrophe.

Commercial and Marine

Business property, cargo and vessels in transit, business interruption, and workers compensation.

Liability and Specialty

Professional indemnity (E&O), D&O, cyber, travel, and parametric insurance products.

Health Insurance

Health insurance covers the cost of medical treatment: hospitalisation, surgery, diagnostics, and in many plans, outpatient and preventive care. In the US this includes employer-sponsored plans and Medicare/Medicaid; in the UK the NHS is supplemented by private health insurers; in Australia the Private Health Insurance Act regulates the market; in India IRDAI governs standalone health insurers.

Individual and Family

Cover for one person, or a shared sum insured across a family. Marketplace and employer plans in the US.

Group Health

Employer-sponsored cover. The largest health segment by premium volume in North America.

Critical Illness and Disability

Lump-sum payout on diagnosis of specified illnesses; income protection on disability.

Government Schemes

Medicare/Medicaid (US), NHS (UK), Medicare (Australia), Ayushman Bharat (India) and top-up plans.

Reinsurance

Reinsurance is insurance for insurance companies. When an insurer accepts a large risk that exceeds its capital capacity, it transfers part of that risk to a reinsurer in exchange for a share of the premium (a “cession”). Global reinsurers include Munich Re, Swiss Re, Hannover Re, General Re, and Lloyd’s of London. IT projects involve premium cession, treaty management, bordereaux reporting, and recovery processing.

Build the insurance knowledge that gets you staffed on projects

Techcanvass’s Insurance Training covers the complete lifecycle, product types, core IT systems, and domain-specific BA and QA scenarios, built for IT and BA professionals with real project context.

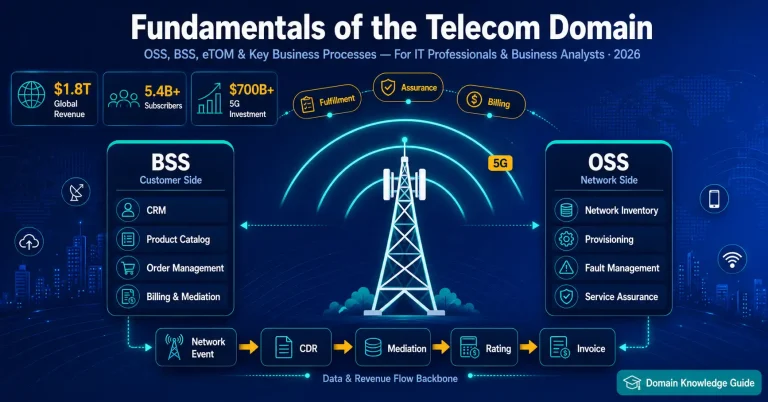

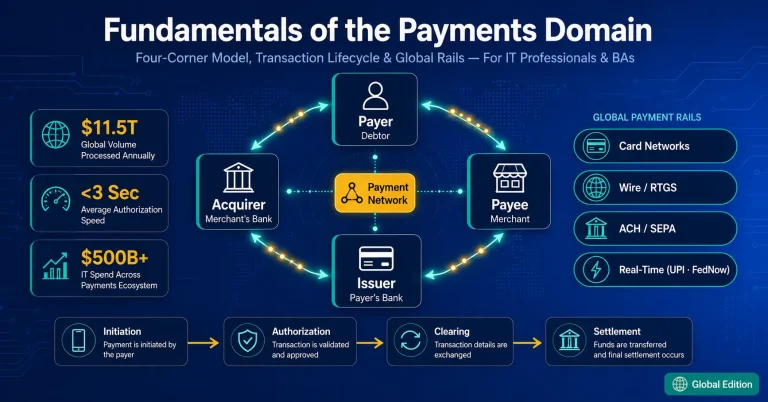

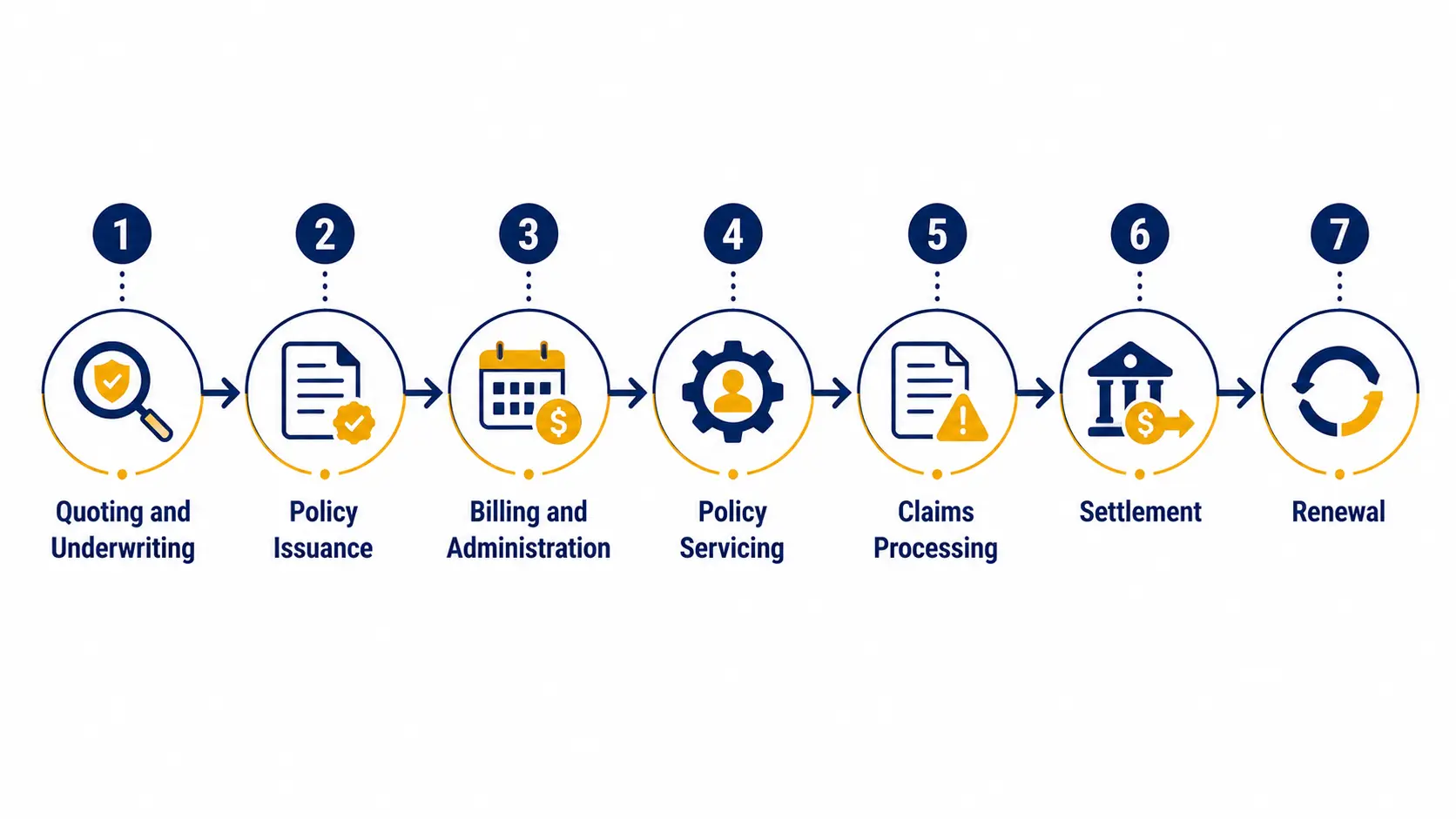

The Insurance Lifecycle: From Quote to Claim

Understanding how insurance policies are administered end to end is the foundation of domain expertise. The lifecycle is consistent across markets, though the systems and regulators differ by country.

| Stage | What Happens | IT / BA Relevance |

|---|---|---|

| 1. Quoting and Underwriting | Applicant data gathered; risk assessed; eligibility and premium calculated | Underwriting workbench, risk-scoring engines, third-party data (credit, telematics, medical) |

| 2. Policy Issuance | Accepted application becomes a policy; contract documents and schedules generated | Policy Administration System (PAS), document generation, e-KYC and digital signature |

| 3. Billing and Administration | Premium collected monthly, quarterly, or annually; endorsements, renewals, and cancellations managed | Premium billing, payment gateways, lapse management, self-service portals |

| 4. Policy Servicing | Mid-term changes: address, sum assured, beneficiary, revival | PAS endorsement workflows, customer portals, broker and agent systems |

| 5. Claims Processing | Insured event occurs; FNOL submitted; loss investigated; coverage verified; compensation determined | Claims Management System, surveyor portals, fraud detection, TPA integrations (health) |

| 6. Settlement and Payout | Verified claim paid to policyholder or beneficiary; subrogation and salvage processed | Payment processing, reinsurance recovery, regulatory reporting |

| 7. Renewal or Lapse | Policy renewed at term end or lapses if premium unpaid; reinstatement workflows | Renewal workflows, lapse triggers, retention analytics |

Actuarial Science underpins the entire lifecycle. Actuaries use statistics and probability to determine the likelihood of future loss events and set premiums that keep the insurer profitable and solvent. When IT projects involve pricing engines or reserve calculations, actuarial teams are key stakeholders a BA must be able to communicate with.

Key Insurance Terminology

Insurance has its own vocabulary, and stakeholders expect you to know it before the first meeting. These are the terms that come up most often across all insurance IT projects.

Parties and the Contract

Insurer (Carrier)

The company underwriting the risk and contractually obligated to pay covered claims.

Insured (Policyholder)

The individual or entity buying insurance coverage and paying the premium.

Policy

The legal contract specifying coverage, exclusions, limits, and terms between insurer and insured.

Beneficiary

The person designated to receive the payout in a life insurance claim.

Premium and Coverage Terms

Premium

The amount the policyholder pays the insurer, typically monthly or annually, to keep the policy active.

Sum Assured / Coverage Limit

The maximum amount the insurer will pay: sum assured in life, coverage limit in P&C and health.

Deductible / Excess

The out-of-pocket amount the insured pays before the insurer covers the remainder.

Exclusion

A condition, scenario, or event explicitly not covered by the policy.

Claims and Risk Terms

Claim

A formal request made by the insured to the insurer for compensation following a covered event.

FNOL

First Notice of Loss: the initial report that a claim event has occurred, triggering the claims workflow.

Risk

The uncertainty or probability of a financial loss occurring; what the insurer prices and accepts.

Underwriting

The process of evaluating, assessing, and classifying risk to decide whether and at what premium to insure.

Financial and Performance Terms

Loss Ratio

Claims paid as a percentage of premiums earned. A ratio above 100% means the insurer pays more than it earns.

Combined Ratio

Loss ratio plus expense ratio. Below 100% indicates underwriting profit; above 100% means underwriting loss.

Reinsurance / Cession

Transferring a portion of accepted risk to a reinsurer in exchange for a share of the premium.

TPA

Third-Party Administrator: manages cashless hospital claims on behalf of health insurers, serving as intermediary between insurer and hospital network.

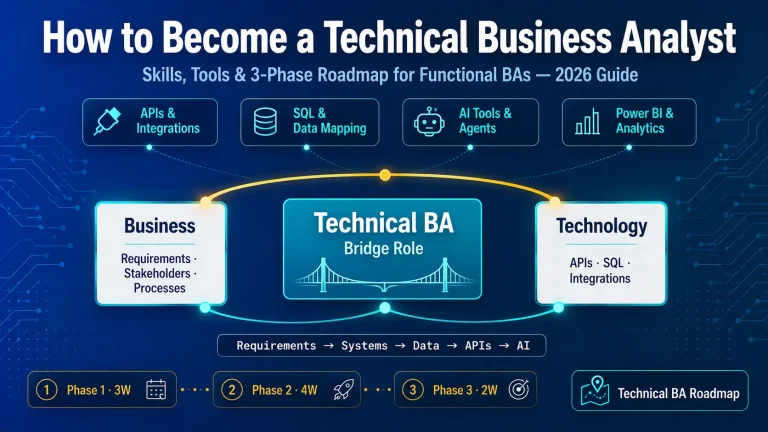

What IT Professionals and Business Analysts Need to Know

Insurance is one of the most complex environments for IT and BA professionals. Policies are legally binding contracts. Regulatory requirements are non-negotiable. Data models are intricate. Here is where domain knowledge creates direct, measurable value:

| Activity | Without Domain Knowledge | With Domain Knowledge |

|---|---|---|

| Requirements elicitation | Misses critical rules: waiting periods, exclusions, rider structures, surrender values | Asks precise questions; understands the full policy lifecycle and edge cases |

| User story writing | Vague stories miss scenarios: lapse/revival, partial withdrawal, paid-up conversion | Complete stories with domain-accurate acceptance criteria |

| Stakeholder communication | Stops to clarify basic terms: FNOL, subrogation, bordereau, treaty | Speaks fluently with underwriters, claims officers, actuaries, and TPA teams |

| Test case design | Generic test cases miss insurance-specific scenarios | Covers premium calculation, sum-assured changes, maturity computation, claim settlement |

| Gap analysis | Cannot map business requirements to system capability | Identifies gaps in PAS functionality versus regulatory or product requirements |

Common IT Projects in the Insurance Sector

- Policy Administration System (PAS) implementation or migration: the most common large-scale insurance IT project globally.

- Claims Management System: life, health, motor, and property claims; including fraud detection and TPA integration.

- Digital distribution platform: online quoting and purchase, e-KYC, agent portal, bancassurance, and telematics.

- Regulatory compliance: Solvency II reporting, IFRS 17 implementation, AML/KYC, NAIC state filings, FCA compliance.

- Analytics and reporting: loss-ratio dashboards, claims trend analysis, premium leakage detection, catastrophe modelling.

- Legacy modernisation: migrating mainframe PAS to modern cloud platforms such as Guidewire, Duck Creek, or Majesco.

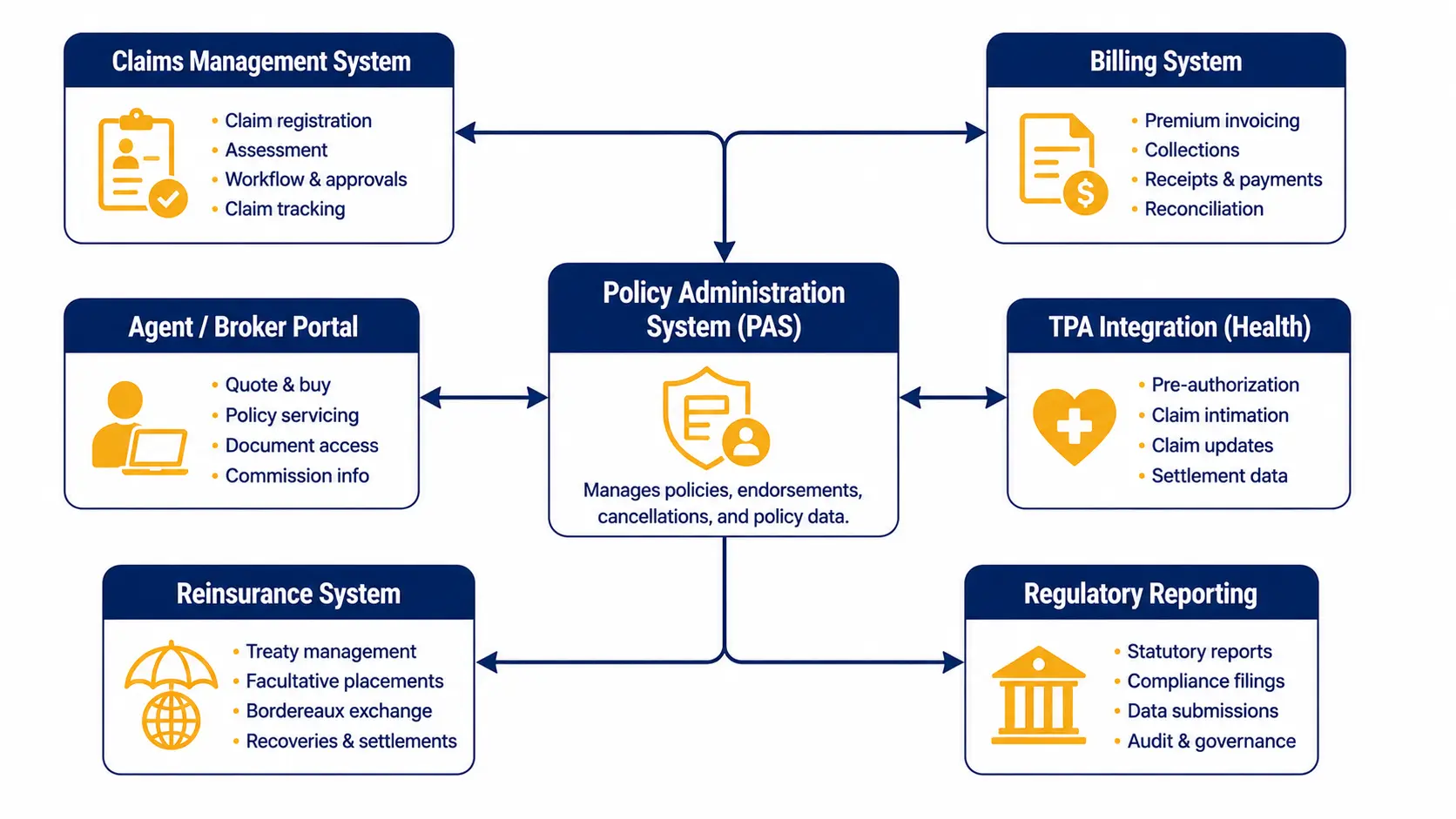

Core Insurance IT Systems

The insurance technology ecosystem has three dominant platform vendors globally (Guidewire, Duck Creek, and Majesco) plus a long tail of legacy systems and regional platforms. Knowing which system handles which function prevents scope confusion and integration design errors.

| System | What It Does | Key Vendors / Examples |

|---|---|---|

| Policy Administration System (PAS) | Core platform managing the full policy lifecycle: quote, underwrite, issue, service, renew, mature | Guidewire PolicyCenter, Duck Creek Policy, Majesco, LifePRO, Oracle OIPA, EbaoTech |

| Claims Management System (CMS) | Manages FNOL, investigation, assessment, settlement, subrogation, and recovery | Guidewire ClaimCenter, Duck Creek Claims, Majesco Claims, Sapiens ClaimsPro |

| Billing and Premium System | Premium invoicing, payment collection, lapse management, and commission accounting | Guidewire BillingCenter, Duck Creek Billing, SAP FSCD |

| Agent and Broker Management | Licensing, onboarding, commission calculation, distribution performance analytics | AgencyBloc, Applied Epic, custom CRM integrations |

| TPA Portal (Health) | Third-Party Administrator manages cashless hospital claims, pre-authorisation, and network billing | HealthEdge, Zelis, Medi Assist (India), MediBuddy |

| Reinsurance System | Cession management, treaty and facultative administration, bordereaux reporting, recovery processing | SAP Reinsurance Management, SICS, Sapiens ALIS |

| Regulatory Reporting and BI | Statutory filings, Solvency II/IFRS 17 reporting, loss-ratio dashboards, fraud analytics | SAS, Moody’s Analytics, Tableau, Power BI, Reltio |

The .insurance TLD: At the infrastructure level, the insurance industry uses the verified .insurance top-level domain, managed by fTLD Registry Services. It mandates strict cryptographic and security protocols (HTTPS, DNSSEC, TLS) to protect consumer data and prevent phishing: a regulatory security requirement IT professionals working in the sector need to be aware of.

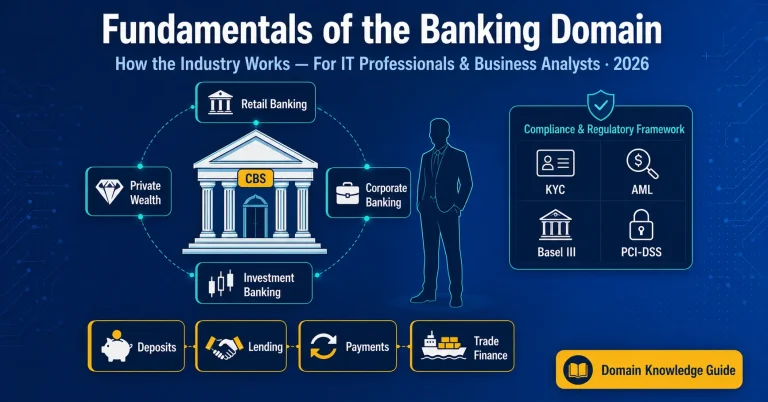

The Insurance Regulatory Landscape

Insurance is one of the most regulation-driven sectors in the world. A large share of insurance IT projects exist solely to meet regulatory requirements. Understanding the key regulators and frameworks is core domain knowledge for anyone working in this sector.

NAIC (US)

State-based regulation coordinated through the National Association of Insurance Commissioners. Each state has its own insurance department.

PRA / FCA (UK)

The Prudential Regulation Authority handles solvency; the Financial Conduct Authority handles conduct and consumer protection.

APRA / ASIC (Australia)

The Australian Prudential Regulation Authority governs capital; ASIC handles market conduct and consumer obligations.

OSFI / Provincial (Canada)

OSFI governs federally regulated insurers; provincial regulators handle most personal lines.

IRDAI (India)

Insurance Regulatory and Development Authority of India governs licensing, product filing, and market conduct.

Solvency II (EU/UK)

Capital adequacy, risk management, and supervisory framework for European insurers; adopted post-Brexit in modified form in the UK.

IFRS 17

Global accounting standard for insurance contracts, replacing IFRS 4. Effective from 2023, significantly impacts financial reporting systems.

AML / KYC and Data Protection

Customer due diligence obligations worldwide: GDPR (EU/UK), DPDP Act (India), Privacy Act (Australia), PIPEDA (Canada).

How to Build Your Insurance Knowledge

You do not need to become an actuary or underwriter. A structured, project-oriented approach works best for IT and BA professionals entering the insurance sector.

Start with the core principles

Understand indemnity, insurable interest, and utmost good faith before anything else. These drive how every system is designed.

Learn the product categories in your market

Know the difference between life, health, and P&C, and which lines your clients operate in. Each has distinct systems, processes, and regulatory obligations.

Map the lifecycle to technology systems

Know what a PAS does, how claims systems differ from billing systems, and which vendors are dominant in your market (Guidewire and Duck Creek in US/UK; Majesco and EbaoTech in Asia).

Learn the regulatory framework for your region

NAIC and state filings in the US, FCA/PRA in the UK, APRA/ASIC in Australia, IRDAI in India, and Solvency II / IFRS 17 across all markets.

Take a structured course with project context

A focused insurance training program closes the gap faster than self-study and adds the practical scenarios you encounter on real projects.

Ready to specialise in BFSI?

Explore Techcanvass’s domain guides and training for IT professionals and Business Analysts who want to win insurance and BFSI projects with confidence.

Frequently Asked Questions

What is the insurance domain?

What are the core principles of insurance?

What are the main types of insurance?

What does a Business Analyst do in the insurance sector?

What is a Policy Administration System (PAS)?

How is insurance regulated differently across the US, UK, Australia, and India?

Explore the Full BFSI Domain

Insurance sits within the broader BFSI sector. These guides connect the full picture for IT professionals and Business Analysts working across the industry.

What Is the BFSI Domain? Full Form, Meaning and Complete Guide

The parent sector explained: how banking, financial services, and insurance connect, and what IT professionals need to know.

Read guide BankingBanking Domain Fundamentals: How the Industry Works

CBS, lending lifecycle, payment rails, Basel III, and the regulatory landscape for banking IT projects globally.

Read guide PaymentsPayments Domain Knowledge: A Complete Guide

How domestic and cross-border payment rails work: RTGS, ACH, Faster Payments, SWIFT, and card networks globally.

Read guide Capital MarketsInvestment Banking Domain Knowledge

Equities, fixed income, derivatives, M&A, and capital markets operations for front-office technology professionals.

Read guide Career GuidanceWhich BA Domain Should You Choose? Banking, Insurance, or Healthcare?

A structured comparison to help IT and BA professionals decide where to build their domain expertise.

Read guide TrainingInsurance Domain Training for IT and BA Professionals

Complete lifecycle, product types, IT systems, and regulatory frameworks with real project scenarios.

View training