What is the BFSI Domain?

Meaning, Sectors & Complete Guide

The BFSI domain is the combined sector of banks, financial services firms, and insurance companies that manage money, credit, and risk globally. Learn the key sub-sectors, core software structures, and pathways for IT & Business Analyst careers.

What is the BFSI Domain?

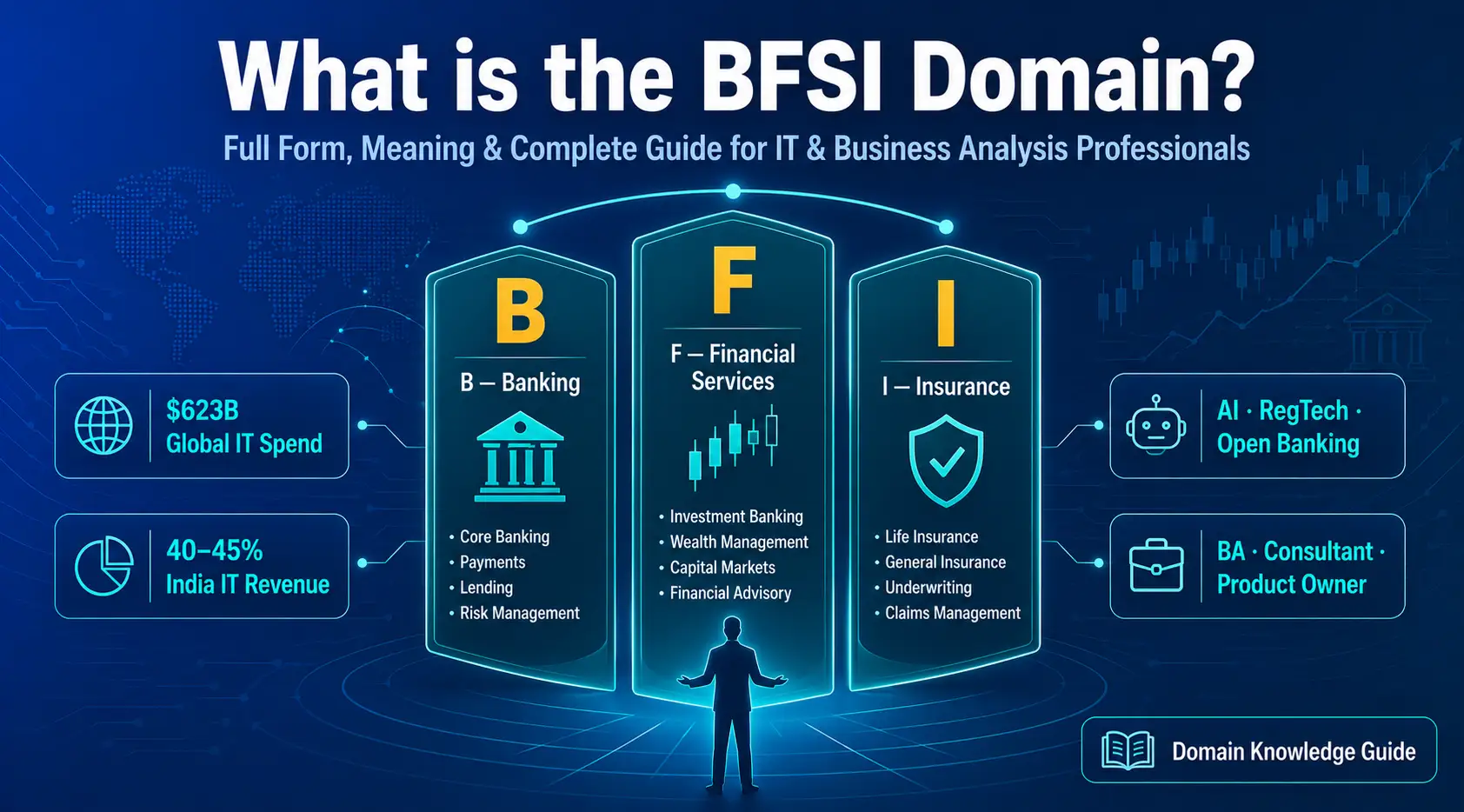

BFSI is the umbrella term for Banking, Financial Services, and Insurance. The BFSI domain is the combined sector of banks, financial-services firms, and insurance companies that manage money, credit, payments, investments, and risk for individuals, businesses, and governments. It accounts for a significant share of global GDP and forms the backbone of the modern economy. In IT, consulting, and business analysis, BFSI refers to this specific industry vertical.

The BFSI domain is one of the most reputed and project-rich verticals in the IT industry. As of 2023, the global BFSI market was valued at $20.5 trillion and is projected to grow at a 6.2% CAGR through 2030 (Source: Grand View Research). India’s BFSI sector alone contributes over 6% of the country’s GDP and is expected to become one of the world’s largest banking markets by 2050.

The BFSI sector is a critical element of the economy. Its organisations enable the accumulation and circulation of capital, allow business owners to expand their businesses, and give individuals the ability to manage and grow their finances. World Bank data shows the financial sector has historically accounted for more than 20% of global GDP, and during the 2008 financial crisis, the resilience of well-regulated BFSI institutions helped limit wider economic damage.

Global BFSI market (2023)

Total value of financial sector activity worldwide (Grand View Research).

Projected CAGR to 2030

Expected annual growth rate of the global BFSI market.

Of India’s IT services revenue

Share of Indian IT services revenue that comes from BFSI clients.

The 3 Sectors of the BFSI Domain

The BFSI domain is divided into three main sectors, each with its own sub-segments, regulatory environment, and technology needs. Understanding each one is essential for IT professionals working on BFSI projects and for Business Analysts gathering requirements from BFSI clients.

The BFSI ecosystem comprises three tightly interconnected sectors: Banking, Financial Services, and Insurance.

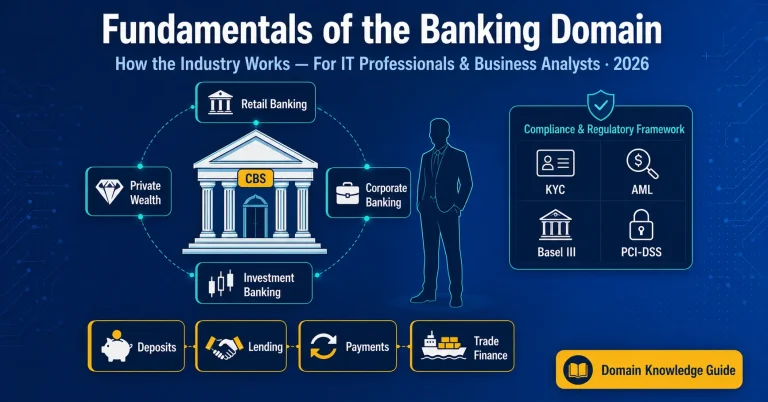

1. Banking

Banking is the core pillar, handling deposits, loans, and transactional services for individuals and enterprises.

Sub-sectors: commercial banks, retail banks, credit unions, cooperative banks, NBFCs, and corporate/investment banks.

The banking sector includes all institutions that accept deposits from the public and extend credit, loans, mortgages, and financing. It is the most regulated sub-sector within BFSI, subject to oversight from central banks and government regulators. Read our complete guide on Banking Domain Knowledge for BAs to learn the core operations.

Retail Banking

Savings, personal loans, home loans, credit cards (B2C)

Corporate / Commercial Banking

Working capital, trade finance, project finance

Investment Banking

IPOs, M&A advisory, capital markets, structured finance

Central Banking

RBI, Federal Reserve — monetary policy, systemic risk

NBFCs & Cooperative Banks

Financial inclusion, rural lending, microfinance

As of 2022, there were approximately 4,500 commercial banks in the US with assets exceeding $24 trillion (Source: Federal Reserve). India has 12 public sector banks, 22 private sector banks, and 46 foreign banks operating across the country (Source: RBI, 2024).

For Business Analysts & IT professionals: Common BFSI banking projects include Core Banking System (CBS) migrations, digital onboarding platforms, loan origination systems (LOS), AML/KYC compliance tools, and payment gateway integrations.

2. Financial Services

Financial Services covers market-facing services focused on managing wealth, capital, and transactions.

Sub-sectors: wealth management, asset management, mutual funds, stock-broking, payment gateways, and fintech.

Financial Services is a broad category covering the intermediaries and platforms that facilitate investment, trading, and capital movement. While banking handles deposits and lending, financial services focus on wealth creation, capital markets, and investment management. To understand investment structures, read our guide on Capital Markets Business Analysis.

Capital Markets

Stock exchanges, bond markets, derivatives, clearing houses

Asset Management

Mutual funds, hedge funds, pension funds, PMS

Payment Systems & Fintech

UPI, digital wallets, BNPL, open banking

Market Utilities

Clearing and settlement platforms that reduce risk

Consumer Credit

Lending platforms, credit scoring, BNPL services

In 2023, the global financial services market was valued at $22.5 trillion (Source: IBISWorld). India’s financial services sector has grown rapidly — UPI alone processed over 100 billion transactions in FY 2023-24 (Source: NPCI).

For Business Analysts & IT professionals: Financial Services projects typically involve trading platforms, portfolio management systems, payment gateway APIs, regulatory reporting (MiFID II, SEBI compliance), and open banking integrations. Concepts like T+1 settlement, NAV calculation, and clearing cycles are critical for BFSI BA work.

3. Insurance

Insurance is the risk-management segment, providing financial protection against unforeseen events.

Sub-sectors: life insurance, term insurance, health insurance, and general (property/casualty) insurance.

The insurance sector manages risk by pooling premiums from many policyholders to cover the financial losses of a few. It is a highly data-intensive industry, premium pricing (actuarial science), claims processing, and fraud detection are all heavily technology-driven. For a deep dive into claims and underwriting, explore our guide on Insurance Domain Knowledge for BAs.

Life Insurance

Term plans, ULIPs, endowment policies, annuities

Health Insurance

Individual, group, and government schemes

General Insurance

Property, motor, marine, travel, liability

Reinsurance

Insurance for insurers — catastrophic risk

InsurTech

Telematics, parametric insurance, AI underwriting

In 2023, the global insurance industry collected over $6.5 trillion in premiums (Source: Swiss Re). India’s insurance penetration stood at around 4% of GDP, significantly below the global average of about 7%, indicating strong room for growth (Source: IRDAI, 2024).

For Business Analysts & IT professionals: Insurance IT projects include Policy Administration Systems (PAS), Claims Management Systems, Bancassurance platforms, actuarial modelling tools, and AI-driven fraud detection. The core process of underwriting to policy issuance to premium collection to claims to settlement must be understood by any BA in this space.

| BFSI Sector | Core Function | Global Size (2023) |

|---|---|---|

| Banking | Deposits, credit, payments | $9.0T in assets (top 10 banks) |

| Financial Services | Investment, trading, capital movement | $22.5T (IBISWorld) |

| Insurance | Risk pooling and protection | $6.5T in premiums (Swiss Re) |

| BFSI Combined | The financial backbone of the economy | $20.5T (Grand View Research) |

Build BFSI Domain Knowledge That Employers Want

Techcanvass offers structured Banking, Insurance, and Payments domain training designed for IT professionals and Business Analysts working on BFSI projects. Learn the processes, terminology, and systems that hiring managers expect.

Why the term BFSI is used

The term BFSI is used most often in IT, consulting, and outsourcing. Because these companies handle highly sensitive data and complex transactions, their software needs specialised business logic. IT and BPO firms group banking, financial services, and insurance together when building software, testing financial applications, and managing customer support under strict regulatory and compliance standards.

Core Systems You’ll Encounter in BFSI Projects

Anyone entering a BFSI development, testing, or analytics workflow will regularly encounter standard corporate platforms. Knowing what they do conceptually makes any IT professional stand out:

-

Core Banking System (CBS)

The centralised backend system that handles a bank’s daily posting transactions, updates balance ledgers, processes interbank clearances, and maintains accounting records (e.g., Finacle, TCS BaNCS, Temenos).

-

Loan Origination System (LOS)

The workflow system that manages consumer and corporate loan applications from customer registration, document capture, and DTI verification up to credit underwriting and automated dispersal.

-

Policy Administration System (PAS)

The central system of record for insurance businesses that manages quotes, active policy portfolios, contract extensions, underwriting rules, premium billing, and renewals.

-

Claims Management System (CMS)

The workflow system that coordinates claims processing, records third-party assessor updates, calculates deductibles, and triggers payouts.

-

Payment Gateways & Processors

Secure routing networks that capture payment token data, verify customer limits with issuing banks, and settle funds with acquiring merchants.

-

Portfolio Management System (PMS)

Advanced trading systems that investment analysts and wealth managers use to execute orders, calculate risk, and calculate mutual fund Net Asset Values (NAV).

BFSI Regulators & Key Regulations

The BFSI sector is highly regulated to protect consumers, prevent fraud, and avoid economic crises. Financial systems must comply with local and international regulations, making compliance knowledge highly valuable for BAs.

| Regulator / Standard | Governance Area | What a BA Must Implement (The Requirement) |

|---|---|---|

| RBI (Reserve Bank of India) | Indian Banking | Mandatory two-factor authentication, KYC verification, and NPA classification timelines. |

| SEBI (India) / SEC (USA) | Capital Markets | Enforcing transaction logs, trade processing audits, and protecting customer investments. |

| IRDAI (India) | Indian Insurance | Solvency margin limits, claims settlement times, and bancassurance distribution rules. |

| Basel III Accords | Global Banking | Bank capital adequacy calculations, liquidity metrics, and stress-testing rules. |

| GDPR / DPDP Act | Data Privacy | Ensuring consent for transactions, secure data storage (tokenization), and handling PII. |

BFSI Sector vs BFSI Industry: What is the Difference?

People often search for “BFSI sector” and “BFSI industry” interchangeably, and in everyday use they mean almost the same thing. There is a subtle distinction worth knowing when you work in the domain.

The BFSI sector means the broad slice of the economy made up of all banking, financial services, and insurance activity, the way economists or governments classify it. The BFSI industry usually refers to the businesses and companies operating within that sector, the way an employer or IT services firm talks about it. So a Business Analyst might say they “work in the BFSI industry” while a policy report discusses “the BFSI sector’s contribution to GDP”.

| Term | Typical Meaning | Used By |

|---|---|---|

| BFSI Sector | The economic segment covering all banking, financial services, and insurance activity | Economists, regulators, policy reports |

| BFSI Industry | The companies and businesses operating within that sector | Employers, IT firms, job descriptions |

| BFSI Domain | The same vertical seen as a knowledge and project area for IT and BA work | IT services, consultants, Business Analysts |

For most practical purposes — especially in IT and business analysis — BFSI sector, BFSI industry, and BFSI domain all point to the same group of banking, financial services, and insurance organisations.

Why the BFSI Domain Matters for IT Professionals and Business Analysts

The BFSI sector is the single largest consumer of IT services globally. According to Gartner, the BFSI sector spent over $623 billion on IT in 2022, with banks alone accounting for $222 billion of that spend. In India, roughly 40-45% of all IT services revenue comes from BFSI clients.

For a Business Analyst or IT professional, this means one thing: BFSI is where the projects are. And in BFSI, domain knowledge is not optional. It is the difference between a BA who can elicit requirements confidently and one who struggles to understand what the business stakeholder is actually asking for.

| Aspect | Without BFSI Domain Knowledge | With BFSI Domain Knowledge |

|---|---|---|

| Requirements Elicitation | Misses critical business rules (KYC norms, NPA classification) | Asks the right questions; understands regulatory constraints immediately |

| Stakeholder Communication | Needs constant explanation of basic terms (AML, CBS, premium, NAV) | Speaks the language of the business; builds instant credibility |

| Solution Design | May propose technically valid but operationally impossible solutions | Understands what the system must do within regulatory and business constraints |

| Test Case Writing | Generic test cases miss domain-specific edge cases | Covers domain scenarios: failed KYC, premium lapse, margin calls |

| Delivery Speed | Slower; more clarification cycles needed | Faster delivery; fewer iterations and reworks |

This is why BFSI domain training has become a near-prerequisite for IT professionals seeking BFSI client projects, whether they work in system integration, product companies, or consulting firms.

Case Study: Loan Origination Flow (With vs. Without Domain Knowledge)

To understand the difference domain knowledge makes, let’s look at a common BFSI project: automating credit approval and onboarding for a digital personal loan app.

The BA WITHOUT Domain Knowledge

This BA approaches the project as a generic IT form: Input User Data → Call Credit Rating API → Check Score → Approve/Reject.

- Misses Hard Pull vs. Soft Pull bureau distinctions, accidentally lowering applicant credit scores during simple rate comparisons.

- Fails to specify how Debt-to-Income (DTI) and FOIR ratios limit borrowing, leading to high-risk automated loan approvals.

- Forgets to include regulatory KYC/AML checks, exposing the bank to compliance audits and financial penalties.

The BA WITH Domain Knowledge

This BA understands risk, credit policies, and central bank regulations, building a secure, automated workflow.

- Uses a Soft Pull to show initial interest rates, running a Hard Pull only after the applicant accepts the final loan terms.

- Builds automated checks for DTI and active default history (NPAs) directly into the credit evaluation logic.

- Integrates central KYC and AML checks (NSDL, CERSAI) into the onboarding flow to prevent identity fraud.

- Designs a manual underwriting queue for marginal cases, avoiding auto-rejecting viable customers.

The difference is clear: domain knowledge helps the Business Analyst build a system that is compliant, secure, and aligned with banking standards, rather than just technically functional.

What is BFSI Domain Knowledge?

BFSI domain knowledge refers to a working understanding of the business processes, regulations, terminology, and systems that operate within the Banking, Financial Services, and Insurance sector. It is not about being a finance expert. It is about know enough of how the BFSI business works that you can do your IT or analytical job effectively within a BFSI environment.

For a Business Analyst, BFSI domain knowledge means:

- Understanding banking products such as loans, deposits, trade finance, letters of credit, and how they are processed.

- Knowing key regulations like KYC, AML, Basel norms, and SEBI or IRDAI guidelines that shape system requirements.

- Speaking the terminology — NAV, NPA, premium, underwriting, settlement, reconciliation — without needing it explained.

- Recognising core systems such as Core Banking Systems, Policy Administration Systems, and payment gateways.

- Mapping end-to-end processes like loan origination or the underwriting-to-claims lifecycle.

The deeper your BFSI domain knowledge, the more confidently you can elicit requirements, write accurate user stories, design realistic solutions, and communicate with business stakeholders as a peer rather than an outsider.

Key Technologies Transforming BFSI in 2025-2026

The BFSI domain is one of the fastest-adopting verticals for new technology, because efficiency, compliance, and customer experience all translate directly into competitive advantage. These are the technologies driving the most BFSI projects today.

AI & Machine Learning

Fraud detection, credit scoring, AI underwriting, chatbots, and intelligent document processing.

Cloud & Core Modernisation

Cloud-native core banking, microservices, and migration off legacy monolithic systems.

Open Banking & APIs

Account aggregation, embedded finance, and third-party integrations via secure APIs.

Digital Payments

UPI, real-time payments, digital wallets, and buy-now-pay-later platforms.

RegTech & Compliance

Automated KYC/AML, regulatory reporting, and risk monitoring tools.

Blockchain & DLT

Trade finance, settlement, and tamper-evident record-keeping pilots.

For Business Analysts, each of these technology shifts creates demand for people who understand both the technology and the underlying BFSI business process it is changing.

BFSI Domain Career Paths and Roles

Because the BFSI domain spans business, technology, and operations, it offers a wide range of roles for people with domain knowledge. Some of the most common BFSI career paths for IT and analysis professionals include:

BFSI Business Analyst

Elicits requirements, writes BRDs and user stories, and bridges banking, insurance, or capital-markets stakeholders with delivery teams.

Domain Consultant / SME

Provides deep banking, payments, or insurance expertise to guide solution design and pre-sales for BFSI clients.

Product Owner / Product Analyst

Owns the backlog for BFSI products such as lending platforms, payment apps, or claims systems.

Risk, Compliance & QA Roles

Tests and validates BFSI systems against regulatory rules, edge cases, and audit requirements.

Across all of these roles, BFSI domain knowledge is the differentiator that moves you from a generalist into a specialist commanding higher demand and stronger compensation.

BFSI BA Salary & Job Demand

BFSI is the single largest consumer of IT services, so qualified Business Analysts with domain knowledge are in strong demand from banks, consulting firms, and IT services providers. Domain expertise carries a real premium: in 2026, BAs working in BFSI, fintech, and digital lending in India typically earn around ₹9-22 LPA, above generic BA roles, because regulatory and risk knowledge is valued more highly (Source: IIT Kanpur / E&ICT). For a fuller breakdown, see our guide on Business Analyst Salary in India & Globally.

| Career Stage | Average Salary (India) | Average Salary (USA) |

|---|---|---|

| Entry-Level BA (0-2 Years) | ₹5.5L – ₹8.0L / Year | $75,000 – $92,000 / Year |

| Middle-Level BA (2-6 Years) | ₹10L – ₹18L / Year | $95,000 – $125,000 / Year |

| Senior BA / Domain SME (6+ Years) | ₹20L – ₹35L / Year | $130,000 – $165,000+ / Year |

Figures are indicative ranges for Business Analyst roles and vary by city, employer, certification, and BFSI sub-domain. Sources: Glassdoor India, Glassdoor US, and AmbitionBox (as of 2026).

How to Build BFSI Domain Knowledge

You do not need a finance degree to build BFSI domain knowledge. A structured, project-oriented approach works best:

Start with one sub-sector

Pick banking, payments, or insurance and learn its core processes end to end before going broad.

Take a structured domain course

A focused BFSI or banking domain training program teaches terminology, processes, and systems in the right sequence.

Practise on realistic scenarios

Write requirements, process maps, and user stories for sample BFSI features such as loan origination or claims processing.

Learn the regulations and systems

Understand KYC/AML, Core Banking Systems, and Policy Administration Systems that recur across BFSI projects.

Ready to specialise in the BFSI domain?

Explore Techcanvass’s Banking, Insurance, and Payments domain guides and training, built for IT professionals and Business Analysts who want to win BFSI projects with confidence.

Key BFSI Terms Every Business Analyst Should Know

The BFSI domain has its own vocabulary, and stakeholders expect you to know it. Here are the terms that come up most often on BFSI projects, in plain language. Bookmark this glossary for interview preparation and requirement workshops.

Banking & Lending Terms

KYC (Know Your Customer)

The mandatory process of verifying a customer’s identity before onboarding.

AML (Anti-Money Laundering)

Rules and checks that stop illegal funds from moving through the system.

NPA (Non-Performing Asset)

A loan on which the borrower has stopped paying interest or principal.

CBS (Core Banking System)

The central software that runs accounts, deposits, and transactions across branches.

LOS (Loan Origination System)

The platform that manages a loan from application to disbursal.

NBFC

A Non-Banking Financial Company that lends but cannot accept demand deposits.

Financial Services & Capital Markets Terms

NAV (Net Asset Value)

The per-unit price of a mutual fund, calculated at the end of each trading day.

T+1 Settlement

Trades settle one business day after the transaction date.

Clearing & Settlement

The process of confirming, matching, and finalising the transfer of money and securities.

AUM (Assets Under Management)

The total market value of investments a fund or manager handles.

UPI

India’s Unified Payments Interface for instant real-time bank-to-bank transfers.

Reconciliation

Matching two sets of records to confirm money and transactions agree.

Insurance Terms

Premium

The amount a policyholder pays to keep an insurance policy active.

Underwriting

Assessing risk to decide whether to insure and at what price.

Claim Settlement

The process of paying out a valid insurance claim to the policyholder.

PAS (Policy Administration System)

The core software that manages policies from issuance to renewal.

Reinsurance

Insurance bought by insurers to limit their exposure to large losses.

Actuarial Science

The use of statistics to price risk and set premiums.