Banking Domain Knowledge: A Complete Guide for IT and Business Analysis Professionals

The banking domain refers to the industry sector encompassing all institutions, processes, systems, and regulations involved in banking — including commercial banks, central banks, cooperative banks, and NBFCs. For IT professionals and Business Analysts, banking domain knowledge means understanding how banks operate as businesses well enough to deliver technology projects for banking clients — gathering accurate requirements, working with core banking systems, and navigating the regulatory landscape that governs every banking IT decision.

In This Article

What is the Banking Domain?

The banking domain is the industry sector encompassing all institutions, processes, products, and regulations involved in the business of banking — accepting deposits, providing credit, facilitating payments, and managing financial risk. It is the largest sub-sector within the BFSI (Banking, Financial Services, and Insurance) sector and one of the most technology-intensive industries in the world.

In IT and Business Analysis, the banking domain is a specific area of industry expertise. Working in the banking domain means having enough knowledge of how banks operate — their products, processes, systems, and regulatory obligations — to effectively deliver technology projects for banking clients. This knowledge is what separates a domain-aware IT professional from one who needs constant hand-holding from business stakeholders.

| Banking Domain at a Glance | |

|---|---|

| Total bank assets in India (2024) | Rs 230+ trillion (RBI) |

| Number of scheduled commercial banks in India | ~100 (public, private, foreign, small finance, payments banks) |

| India’s banking sector IT spend | $10+ billion annually |

| Primary regulator in India | Reserve Bank of India (RBI) |

| Key India banking technology associations | IBA (Indian Banks’ Association), IDRBT |

| Primary IT roles in banking | Business Analyst, Core Banking Consultant, QA Engineer, Data Analyst, Product Manager |

What is Banking Domain Knowledge?

Banking domain knowledge is a working understanding of how the banking business operates — its products, processes, regulatory requirements, and technology systems — sufficient to perform an IT or Business Analysis role within a banking environment.

It is not the same as having a banking qualification or a finance degree. A BA or IT professional with banking domain knowledge does not need to understand actuarial models or treasury operations in depth — they need to understand the business well enough to ask the right questions, interpret stakeholder requirements correctly, and design solutions that fit within how banks actually work.

| Domain Knowledge Area | What It Covers | Why IT/BA Professionals Need It |

|---|---|---|

| Banking Products | Savings accounts, current accounts, fixed deposits, personal loans, home loans, credit cards, trade finance, forex | To understand the data model of core banking systems and the business context of every requirement |

| Banking Processes | Account opening, KYC, loan origination, loan servicing, payments processing, trade finance, collections | End-to-end process understanding is essential for requirement elicitation, gap analysis, and test design |

| Core Banking Systems | Finacle, FLEXCUBE, T24/Temenos Transact, FinnOne, BaNCS — what they do, how they are configured | Knowing which system owns which function prevents scope confusion and integration design errors |

| Regulations and Compliance | RBI guidelines, Basel III/IV, KYC/AML, FATCA, FEMA, Priority Sector Lending norms | Regulatory requirements drive a large percentage of banking IT projects — non-negotiable domain knowledge |

| Banking Terminology | NPA, CRAR, SLR, CRR, CASA, LAP, NIM, ALM, IFSC, SWIFT, Nostro/Vostro | Using correct terminology builds credibility with banking stakeholders immediately |

| Banking Data | Customer data, transaction data, loan portfolio data, regulatory reporting data | Data projects require knowledge of what banking data represents and how it is structured in CBS |

Techcanvass’s Banking Domain Training is designed specifically for IT professionals and Business Analysts — covering the complete banking lifecycle, products, core systems, and regulatory landscape.

The Indian Banking System — Structure and Types of Banks

The Indian banking system is regulated by the Reserve Bank of India (RBI) and consists of multiple categories of banks, each with distinct mandates, products, and technology requirements. Understanding which category, a client bank belongs to is the starting point for any banking IT project.

| Bank Type | Examples | Primary Focus | IT/BA Relevance |

|---|---|---|---|

| Public Sector Banks (PSBs) | SBI, PNB, Bank of Baroda, Canara Bank | Government-owned. Mass-market retail and corporate banking. Priority sector lending. | Large-scale CBS implementations; government scheme integrations; legacy modernisation projects |

| Private Sector Banks | HDFC Bank, ICICI Bank, Axis Bank, Kotak Mahindra | Technology-first. Retail, corporate, wealth management, cards. | Highest IT investment; digital banking platforms; API banking; analytics projects |

| Foreign Banks | Citibank, Standard Chartered, HSBC, Deutsche Bank | Corporate banking, trade finance, treasury. Limited retail presence. | SWIFT integrations, trade finance systems, global regulatory compliance (FATCA, CRS) |

| Small Finance Banks | AU Small Finance, Equitas, Ujjivan | Financial inclusion — small borrowers, microfinance, unbanked. | Mobile-first platforms; PMJDY integrations; NACH mandate systems; microfinance LOS |

| Payments Banks | Airtel Payments Bank, India Post Payments Bank, Jio Payments Bank | Deposits and payments only — no lending. Mobile-first. | UPI integration, AEPS, BBPS — focused purely on payments technology |

| Regional Rural Banks (RRBs) | Gramin Bank, Aryavart Bank | Rural lending, agricultural credit, government schemes. | CBS implementations — often on Finacle or BaNCS; PMFBY, KISAN credit card systems |

| Cooperative Banks | Saraswat Bank, COSMOS Bank | Member-owned. Urban cooperative banks focus on retail; state cooperative banks on agriculture. | Smaller-scale CBS; RBI digital banking compliance projects; audit and reporting systems |

| NBFCs | Bajaj Finance, Muthoot Finance, HDFC Ltd (erstwhile) | Non-banking financial companies — lending without deposit licence. | Loan Management Systems (LMS), NBFC-specific RBI compliance, co-lending platform integrations |

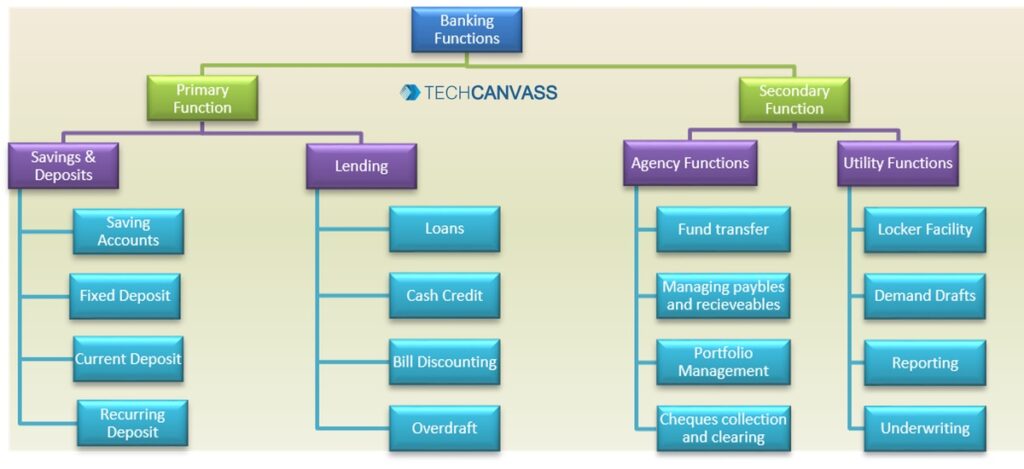

Core Functions of Banks

Banks perform a wide range of functions that can be grouped into primary banking functions — the core deposit and credit activities — and secondary functions including payment services, agency activities, and utility services. For IT professionals, each function corresponds to a system or module that forms the scope of banking technology projects.

Primary Functions

| Function | What It Means | Key IT Systems / BA Projects |

|---|---|---|

| Deposit Acceptance | Banks accept deposits from individuals and businesses — savings accounts, current accounts, fixed deposits, recurring deposits. These deposits form the bank’s primary funding source. | Core Banking System (CBS) — account management module; KYC/AML onboarding; interest calculation engine; digital account opening |

| Lending and Credit | Banks deploy deposits as loans — personal loans, home loans, auto loans, business loans, credit cards, overdrafts, trade finance. Interest income on loans is the primary revenue source. | Loan Origination System (LOS); Loan Management System (LMS); credit scoring integration; collections and recovery system; NPA management module |

| Liquidity Management | Banks maintain regulatory reserves (CRR, SLR) and manage liquidity to meet withdrawal demands and regulatory requirements. | Treasury Management System; ALM (Asset-Liability Management) system; regulatory reporting — RBI returns |

Secondary Functions

| Function | What It Means | Key IT Systems / BA Projects |

|---|---|---|

| Payments and Settlements | Facilitating money transfer — NEFT, RTGS, IMPS, UPI, SWIFT, demand drafts, cheque clearing (CTS) | Payment Hub; NPCI integrations (UPI, IMPS, NACH); SWIFT messaging; CTS infrastructure |

| Agency Functions | Acting on behalf of customers — collecting payments, managing investments, transferring funds, tax payments, dividend collection. | Bancassurance platforms; mutual fund distribution; tax payment integrations (OLTAS, GST) |

| Trade Finance | Financing international trade — letters of credit (LC), bank guarantees (BG), export bill discounting, forex remittances. | Trade Finance System; SWIFT LC/BG messaging; forex deal management; correspondent banking |

| Wealth Management | Investment advisory, portfolio management, demat services, mutual funds, insurance products for HNI customers. | Wealth management platforms; demat integrations (NSDL/CDSL); robo-advisory tools |

| Utility Services | Safe deposit lockers, demand drafts, notary services, investment custody, reporting. | Ancillary CBS modules; document management systems; reporting and MIS platforms |

Core Banking Systems — What IT Professionals Need to Know

A Core Banking System (CBS) is the central technology platform that manages a bank’s primary operations — customer accounts, deposits, loans, transactions, and interest calculations — in real time across all channels and branches. CBS is the most important technology system in any bank and is the subject of the most significant banking IT projects.

| CBS Platform | Vendor | Market Presence | Common Project Types |

|---|---|---|---|

| Finacle | Infosys | Dominant in India — SBI, Bank of Baroda, many PSBs and cooperative banks | CBS implementation, Finacle upgrade, digital banking integration, API banking on Finacle |

| FLEXCUBE (OFSS) | Oracle Financial Services (OFSS) | Large presence in India and globally — ICICI Bank, many mid-size banks | FLEXCUBE implementation, upgrade projects, custom module development, reporting |

| Temenos Transact (T24) | Temenos | Strong in global and private banks, growing in India | T24 implementation, upgrade to Transact, cloud migration projects |

| BaNCS | TCS Financial Solutions | SBI (partial), cooperative banks, international banks | CBS implementation, BaNCS payments module, trade finance on BaNCS |

| FinnOne Neo | Nucleus Software | Leading in NBFC and lending — Bajaj Finance, many NBFCs | LMS implementation on FinnOne, co-lending module, collections system |

| Mambu / nCino | Cloud-native vendors | New-age banks, small finance banks, digital lenders | Cloud-native CBS implementation, digital onboarding, API-first architecture |

For Business Analysts working on CBS projects, understanding the functional modules of a core banking system is essential:

| CBS Platform | Vendor | Market Presence | Common Project Types |

|---|---|---|---|

| Finacle | Infosys | Dominant in India — SBI, Bank of Baroda, many PSBs and cooperative banks | CBS implementation, Finacle upgrade, digital banking integration, API banking on Finacle |

| FLEXCUBE (OFSS) | Oracle Financial Services (OFSS) | Large presence in India and globally — ICICI Bank, many mid-size banks | FLEXCUBE implementation, upgrade projects, custom module development, reporting |

| Temenos Transact (T24) | Temenos | Strong in global and private banks, growing in India | T24 implementation, upgrade to Transact, cloud migration projects |

| BaNCS | TCS Financial Solutions | SBI (partial), cooperative banks, international banks | CBS implementation, BaNCS payments module, trade finance on BaNCS |

| FinnOne Neo | Nucleus Software | Leading in NBFC and lending — Bajaj Finance, many NBFCs | LMS implementation on FinnOne, co-lending module, collections system |

| Mambu / nCino | Cloud-native vendors | New-age banks, small finance banks, digital lenders | Cloud-native CBS implementation, digital onboarding, API-first architecture |

Retail Banking vs Corporate Banking

Banks are generally organised into two primary business divisions — Retail Banking and Corporate Banking (also called Wholesale Banking). Understanding this distinction is important for IT professionals because the technology systems, processes, and regulatory requirements differ significantly between the two.

| Dimension | Retail Banking | Corporate Banking |

|---|---|---|

| Customers | Individual consumers, salaried employees, small business owners | Large corporates, SMEs, government entities, financial institutions |

| Products | Savings accounts, personal loans, home loans, credit cards, FDs, demat | Term loans, working capital, trade finance, treasury, forex, structured finance |

| Transaction volume | Very high volume, low-value transactions | Lower volume, very high-value transactions |

| Key IT systems | CBS account module, LOS, digital banking app, credit scoring | Corporate banking portal, trade finance system, treasury management, SWIFT |

| Regulatory focus | KYC, consumer protection, priority sector lending, fair lending | Large exposure framework, Basel III capital requirements, FEMA, trade compliance |

| BA project examples | Digital onboarding, mobile banking, credit card system, home loan LOS | Trade finance system, corporate internet banking, treasury management, LC/BG issuance |

Other Key Banking Segments

- SME / MSME Banking: Small and medium enterprise lending — a growing segment with government scheme integrations (CGTMSE, Mudra). LOS projects with unique scoring models.

- Agricultural / Priority Sector Banking: Mandatory RBI requirements — 40% of Adjusted Net Bank Credit must go to priority sectors. NABARD tie-ups, PMFBY crop insurance, Kisan Credit Card systems.

- NRI Banking: Non-Resident Indian accounts (NRE/NRO/FCNR), remittances, FEMA compliance. Common IT projects: NRI digital banking portal, remittance platform integrations.

- Wealth Management / Private Banking: High Net Worth Individual (HNI) services — investment advisory, portfolio management, demat, insurance. Wealth platform implementations are growing in large private banks.

Lending Domain Knowledge

Lending — providing credit to individuals and businesses — is the primary revenue-generating activity of banks. For IT professionals, the lending domain is one of the most project-intensive areas of banking, spanning loan origination, credit underwriting, loan management, collections, and regulatory reporting.

The Lending Lifecycle

| Stage | What Happens | IT System Involved |

|---|---|---|

| 1. Lead / Application | Customer applies for a loan — via branch, digital app, or DSA channel | LOS (Loan Origination System) — application capture, document upload, lead management |

| 2. Credit Assessment / Underwriting | Bank assesses creditworthiness — income verification, credit bureau check (CIBIL/Experian), collateral valuation, risk scoring | Credit Bureau integration (CIBIL, Experian, Equifax); credit scoring engine; appraisal tools |

| 3. Sanction / Approval | Credit committee approves the loan — sets amount, rate, tenure, conditions | LOS workflow engine — approval hierarchy, digital signatures, sanction letter generation |

| 4. Documentation | Legal documents executed — loan agreement, mortgage deed, hypothecation | Document Management System; eSign integration; legal verification |

| 5. Disbursement | Loan amount credited to customer account or paid to third party (builder, dealer) | CBS disbursement module; payment to third-party integration; disbursement reconciliation |

| 6. Loan Servicing | EMI collection, prepayment, interest rate change, top-up loan, statement generation | Loan Management System (LMS) — EMI schedule, prepayment calculation, account statements |

| 7. Collections and Recovery | For overdue accounts — reminder calls, legal notices, NPA classification, recovery | Collections system; NPA management module; SARFAESI compliance; recovery agent management |

Key Lending Products IT Professionals Encounter

- Retail Lending: Home loans, personal loans, auto loans, education loans, gold loans — each has unique LOS rules, documentation, and LMS configuration.

- Credit Cards: Revolving credit — card management system, credit limit management, billing cycle, EMI conversion, reward points.

- Corporate Lending: Term loans, working capital (cash credit, overdraft), bill discounting — corporate banking portal, complex covenants.

- Agricultural / Kisan Credit Card: Government-mandated agricultural lending — PMKSY integration, crop insurance linkage, seasonal disbursement rules.

- Co-lending / NBFC partnerships: Banks co-lend with NBFCs under RBI’s co-lending model — complex integration between bank CBS and NBFC LMS.

Key Lending Terms for IT/BA Professionals: LTV (Loan-to-Value ratio), EMI (Equated Monthly Instalment), NPA (Non-Performing Asset), GNPA/NNPA, PCR (Provision Coverage Ratio), CIBIL score, DPD (Days Past Due), SARFAESI Act, IBC (Insolvency and Bankruptcy Code), Priority Sector Lending (PSL).

Banking Domain for Business Analysts

Banking is one of the most complex and rewarding domains for Business Analysts. Every banking product is a legally binding contract subject to regulatory oversight. Every IT project has compliance implications. Domain knowledge is not optional — it directly determines whether a BA can gather complete requirements, identify regulatory constraints, and deliver projects that banks can actually use.

| BA Responsibility | Without Banking Domain Knowledge | With Banking Domain Knowledge |

|---|---|---|

| Requirements elicitation | Misses critical banking rules — interest calculation methods, NPA provisioning, regulatory return formats | Asks precise questions about product configuration, processing rules, regulatory implications |

| User story writing | Generic stories miss banking-specific scenarios — premature closure penalty, dormant account, lien marking | Writes complete stories with banking-accurate acceptance criteria and edge cases |

| Stakeholder communication | Needs explanation of every term — CASA, NPA, SARFAESI, IFRS 9, Basel III | Speaks confidently with branch managers, credit teams, compliance officers, treasury teams |

| Gap analysis | Cannot identify what the existing CBS cannot do vs what the requirement needs | Maps requirements against CBS module capabilities; identifies configuration vs development gaps |

| Regulatory requirements | Misses RBI circular implications; regulatory deadlines; data format requirements | Identifies which requirements are regulatory-driven; flags non-negotiable compliance constraints |

Common Banking IT Projects BAs Work On:

- CBS Implementation / Migration — Moving to a new core banking platform (Finacle, FLEXCUBE, T24) — the largest and most complex banking IT project

- Digital Banking Platform — Retail internet banking, mobile banking app, corporate banking portal

- Loan Origination System (LOS) — End-to-end digital loan application and sanction workflow

- KYC / AML System — Customer due diligence, transaction monitoring, STR/CTR reporting

- Regulatory Reporting — RBI returns, CRILC reporting, Basel III capital adequacy, FATCA/CRS reporting

- Payment Hub Implementation — Centralising NEFT, RTGS, IMPS, UPI, SWIFT into a single payment orchestration layer

- CBS Data Migration — Migrating customer, account, and loan data from legacy system to new CBS — extremely complex BA work

- Open Banking / API Banking — Building account aggregator integrations, API gateway for fintech partnerships

Techcanvass’s Banking Domain Training is designed specifically for Business Analysts and IT professionals — covering the complete banking lifecycle, CBS systems, and real project scenarios.

Banking Domain for QA Testers

Quality Assurance professionals working on banking IT projects require the same domain knowledge as Business Analysts — but applied to test design rather than requirements. A QA tester without banking domain knowledge will write generic test cases that miss the banking-specific business rules that matter most.

| Testing Area | Banking-Specific Test Scenarios | Domain Knowledge Required |

|---|---|---|

| CBS Testing | Interest calculation accuracy; EOD/SOD batch processing; account balance after reversal; dormancy rules | Interest accrual methods (simple vs compound); banking EOD process; dormancy thresholds |

| Loan System Testing | EMI calculation for different rate types; prepayment penalty calculation; NPA classification trigger; moratorium handling | EMI formula; reducing balance vs flat rate; NPA DPD thresholds; moratorium regulatory rules |

| Payment Testing | NEFT/RTGS cut-off times; IMPS 24×7 validation; UPI transaction limits; SWIFT message format validation | Payment system operating hours; NPCI transaction limits; ISO 20022/MT message formats |

| Regulatory Reporting Testing | RBI return format validation; Basel III calculation accuracy; FATCA field completeness; CIBIL reporting format | RBI return formats; Basel III capital calculation; CIBIL data format specification |

| KYC/AML Testing | PEP screening; transaction monitoring rule triggers; STR generation threshold; customer risk rating | FATF risk categories; RBI KYC master direction; transaction monitoring rule logic |

| Cards Testing | Interchange fee calculation; chargeback processing; reward points accrual; 3DS authentication flow | Card scheme rules (Visa/Mastercard/RuPay); PCI DSS scope; chargeback reason codes |

Key IT Systems in Banking

| System | What It Does | Common Vendors / Examples |

|---|---|---|

| Core Banking System (CBS) | Manages all banking products — accounts, loans, transactions, interest, GL | Finacle (Infosys), FLEXCUBE (Oracle), T24/Temenos Transact, BaNCS (TCS) |

| Loan Origination System (LOS) | End-to-end digital loan application, credit assessment, sanction workflow | Newgen LOS, Nucleus FinnOne, Salesforce Financial Services Cloud, custom builds |

| Loan Management System (LMS) | Post-disbursement loan servicing — EMI, prepayment, foreclosure, NPA | Nucleus FinnOne Neo, Oracle LMS, CBS loan module |

| Payment Hub | Centralises all payment types — NEFT, RTGS, IMPS, UPI, SWIFT, NACH | TCS BaNCS Payments, Finastra Fusion Payments, Oracle Payment Hub, Temenos Payments |

| Treasury Management System | Manages treasury operations — forex, money market, bonds, derivatives, ALM | Murex, Finastra Opics, Kondor+, FIS Quantum |

| Trade Finance System | Manages LC, BG, export bills, import collections, forex remittances | Finastra Trade Innovation, Surecomp DOKA, Bolero, CBS trade module |

| KYC / AML System | Customer due diligence, PEP screening, transaction monitoring, STR generation | NICE Actimize, Oracle FCCM, SAS AML, Finacus (India) |

| Digital Banking Platform | Internet banking, mobile banking app, corporate banking portal | Backbase, Temenos Infinity, Infosys BankFusion, custom React/Angular builds |

| Regulatory Reporting System | Generates RBI returns, Basel III reports, CRILC, FATCA/CRS submissions | Wolters Kluwer OneSumX, Moody’s Analytics, custom reporting on CBS data |

| Data Warehouse / Analytics | Customer analytics, risk analytics, branch performance, fraud detection | Teradata, Oracle, Hadoop/Spark ecosystem, Tableau, Power BI on banking data |

Banking Regulatory Landscape

| Regulation / Framework | Issued By | What It Covers | IT Project Implication |

|---|---|---|---|

| RBI Master Directions | Reserve Bank of India | Comprehensive regulations on KYC, AML, lending, digital banking, cybersecurity, payments | Most banking IT projects are driven by or must comply with RBI directions |

| Basel III / IV | Basel Committee (RBI implementation) | Capital adequacy (CRAR), liquidity (LCR, NSFR), leverage ratio, credit risk | Capital calculation engine; regulatory reporting; stress testing platforms |

| KYC Master Direction | RBI | Know Your Customer — customer identification, CDD, periodic KYC update, risk categorisation | KYC onboarding system; periodic KYC review workflows; risk scoring; CKYC integration |

| PMLA / AML Guidelines | Government / FIU-IND | Anti-money laundering — transaction monitoring, STR/CTR reporting to FIU | AML transaction monitoring system; STR/CTR generation; PEP/sanctions screening |

| FATCA / CRS | US IRS / OECD (RBI implementation) | Foreign account tax compliance — reporting US persons’ accounts; global tax information exchange | FATCA self-certification; CRS reportable accounts identification; automated tax reporting |

| RBI Digital Banking Guidelines | RBI | Internet banking security, mobile banking, payment aggregators, account aggregators | MFA implementation; security audit; account aggregator API compliance |

| Priority Sector Lending (PSL) | RBI | Mandates 40% of ANBC to priority sectors — agriculture, MSME, housing, education | PSL tracking system; sub-target monitoring; IBPC/PSL certificates |

| FEMA | RBI / Government | Foreign Exchange Management — NRI accounts, cross-border transactions, forex limits | NRE/NRO account rules; forex transaction monitoring; SWIFT compliance |

Banking Domain Terminology Glossary

The following terms appear regularly in banking IT projects and stakeholder conversations. A BA or IT professional who knows these terms does not need to stop and ask for explanations — which directly builds credibility and project efficiency.

| Term | What It Means | Where IT/BA Professionals Encounter It |

|---|---|---|

| CASA | Current Account Savings Account ratio — proportion of low-cost deposits to total deposits. Higher CASA = lower cost of funds. | Core banking reporting; bank profitability analysis; CBS dashboard projects |

| NPA | Non-Performing Asset — a loan where interest or principal has not been paid for 90+ days. Classified as Sub-Standard, Doubtful, or Loss. | NPA management module in LMS; provisioning calculations; RBI NPA reporting (CRILC) |

| CRAR | Capital to Risk-weighted Assets Ratio — minimum capital a bank must hold relative to its risk exposure. RBI minimum is 9%. | Basel III capital calculation engine; regulatory capital reporting |

| CRR / SLR | Cash Reserve Ratio / Statutory Liquidity Ratio — mandatory reserves banks must maintain with RBI (CRR) or in approved securities (SLR). | Treasury management system; daily liquidity reporting; CBS reserve maintenance |

| KYC / CDD | Know Your Customer / Customer Due Diligence — identity verification and risk assessment of customers before onboarding. | KYC system; CIF creation workflow; periodic review triggers; CKYC integration |

| AML / CFT | Anti-Money Laundering / Countering Financing of Terrorism — transaction monitoring and suspicious activity reporting. | AML system; STR/CTR filing module; sanctions screening; transaction monitoring rules |

| LTV | Loan-to-Value ratio — loan amount as a percentage of collateral value. Regulated by RBI for home loans. | LOS collateral valuation; LTV calculation; eligibility rules engine |

| SWIFT | Society for Worldwide Interbank Financial Telecommunication — global messaging network for cross-border payments. Uses MT/MX message formats. | SWIFT gateway integration; MT103/MT202 message processing; ISO 20022 migration projects |

| IFSC | Indian Financial System Code — 11-character code identifying each bank branch for NEFT/RTGS/IMPS routing. | Payment routing logic; IFSC validation in payment systems; CBS branch master |

| CBS | Core Banking System — the central platform managing all banking operations in real time across all branches and channels. | Every major banking IT project either runs on or integrates with CBS |

| EMI | Equated Monthly Instalment — fixed monthly payment on a loan comprising both principal and interest. | LOS/LMS EMI calculation engine; amortisation schedule; prepayment recalculation |

| Nostro / Vostro | Nostro = our account held with a foreign bank. Vostro = foreign bank’s account held with us. Used in cross-border payments. | Correspondent banking reconciliation; SWIFT payment routing; forex settlement |

Indian Banking Evolution — A Brief Timeline

Understanding India’s banking evolution provides context for why the current regulatory framework exists and why certain banking practices are the way they are — useful background for IT professionals working on regulatory compliance projects.

| Year | Milestone | Significance for IT/BA Professionals |

|---|---|---|

| 1770 | Bank of Hindustan established in Calcutta — first bank in India | Historical starting point — India’s banking system is over 250 years old |

| 1806-1843 | Bank of Calcutta (1806), Bank of Bombay (1840), Bank of Madras (1843) established | Three Presidency Banks — precursors to modern State Bank of India |

| 1921 | Three Presidency Banks merged as Imperial Bank of India | First large-scale banking consolidation in India |

| 1935 | Reserve Bank of India (RBI) established | India’s central bank and primary banking regulator — RBI issues all regulations IT projects must comply with |

| 1955 | Imperial Bank of India renamed State Bank of India (SBI) | SBI becomes India’s largest public sector bank — CBS at SBI runs on Finacle |

| 1969 & 1980 | 14 banks nationalised (1969); 6 more nationalised (1980) | Public sector banks dominate India’s banking landscape — largest CBS implementation projects |

| 1982 | NABARD and EXIM Bank established | Specialised development banks — NABARD for agriculture (PMFBY, KCC), EXIM for trade finance |

| 1991 | Liberalisation — ICICI, HDFC, Axis, IndusInd given banking licences | New private banks drove technology adoption — ICICI and HDFC were among first CBS adopters |

| 2004-2010 | Core Banking Systems deployed across most Indian banks | Largest wave of CBS implementation projects in India — Finacle and FLEXCUBE dominance established |

| 2012-Present | Digital banking, UPI (2016), Account Aggregator (2021), CBDC pilot (2022) | Ongoing wave of digital transformation projects — highest current IT project demand |

How to Build Banking Domain Knowledge

Building banking domain knowledge as an IT professional means acquiring the practical understanding of banking that makes you effective on projects — not becoming a banker. Here is a structured pathway:

Step 1 — Learn the Banking Business

Start with how banks make money — the deposit-lending spread, fee income, treasury returns. Understand the difference between retail and corporate banking, and what types of IT projects each segment generates.

Step 2 — Understand Core Banking Systems

Know the major CBS platforms — Finacle, FLEXCUBE, T24, BaNCS. Understand what each module does (deposits, loans, payments, GL) and what kind of project work each module generates. Even without hands-on CBS access, knowing the landscape prevents scope confusion.

Step 3 — Learn the Lending Domain

Lending is the largest banking IT project category. Understand the lending lifecycle from application through NPA management. Know the key systems — LOS, LMS — and the key terms: EMI, LTV, NPA, DPD, SARFAESI.

Step 4 — Understand the Regulatory Framework

RBI issues the regulations that drive most banking IT projects. Understand the key frameworks: KYC/AML, Basel III, Priority Sector Lending, digital banking guidelines. You do not need to memorise every RBI circular — you need to know which type of project triggers which regulatory requirement.

Step 5 — Get Structured Domain Training

Self-study covers the basics but misses the project-specific context that matters most. Structured banking domain training designed for IT/BA professionals closes that gap faster and more completely.

Conclusion

Banking domain knowledge is one of the most valuable skills an IT professional or Business Analyst can develop. The banking sector — spanning retail banking, corporate banking, lending, payments, trade finance, and treasury — is the largest consumer of IT services in India and one of the most complex domain environments in the world.

The foundation is the same regardless of which banking sub-segment you work in: understand the banking business and its products, know the core banking systems and their modules, understand the lending lifecycle, learn the regulatory framework, and build your terminology. A BA or IT professional with genuine banking domain knowledge delivers better requirements, faster — and that is what the industry rewards.

Ready to build your banking domain knowledge? Techcanvass’s Banking Domain Training is designed specifically for IT professionals and Business Analysts — covering core banking, lending, regulatory frameworks, and real project scenarios.