Fundamentals of the Banking Domain: How the Industry Works

A practical guide to how the banking sector operates, covering primary segments, core products, regulatory frameworks, financial instruments, and technology systems. Relevant for IT professionals and Business Analysts worldwide.

What is the banking domain?

The banking domain covers all institutions, products, processes, and regulations involved in accepting deposits, providing credit, and facilitating payments. It is the largest sector within BFSI and one of the most technology-intensive industries in the world.

For IT professionals and Business Analysts, working in this domain means understanding how banks operate well enough to gather accurate requirements, design compliant solutions, and communicate as a peer with banking stakeholders, without needing a finance degree.

What this guide covers

- 1Primary banking segments: retail, corporate, investment, private

- 2Core products and services: deposits, lending, payments, trade finance

- 3Regulatory and compliance frameworks: KYC, AML, Basel

- 4Financial instruments and markets

- 5Technology systems: CBS, LOS, payment hubs

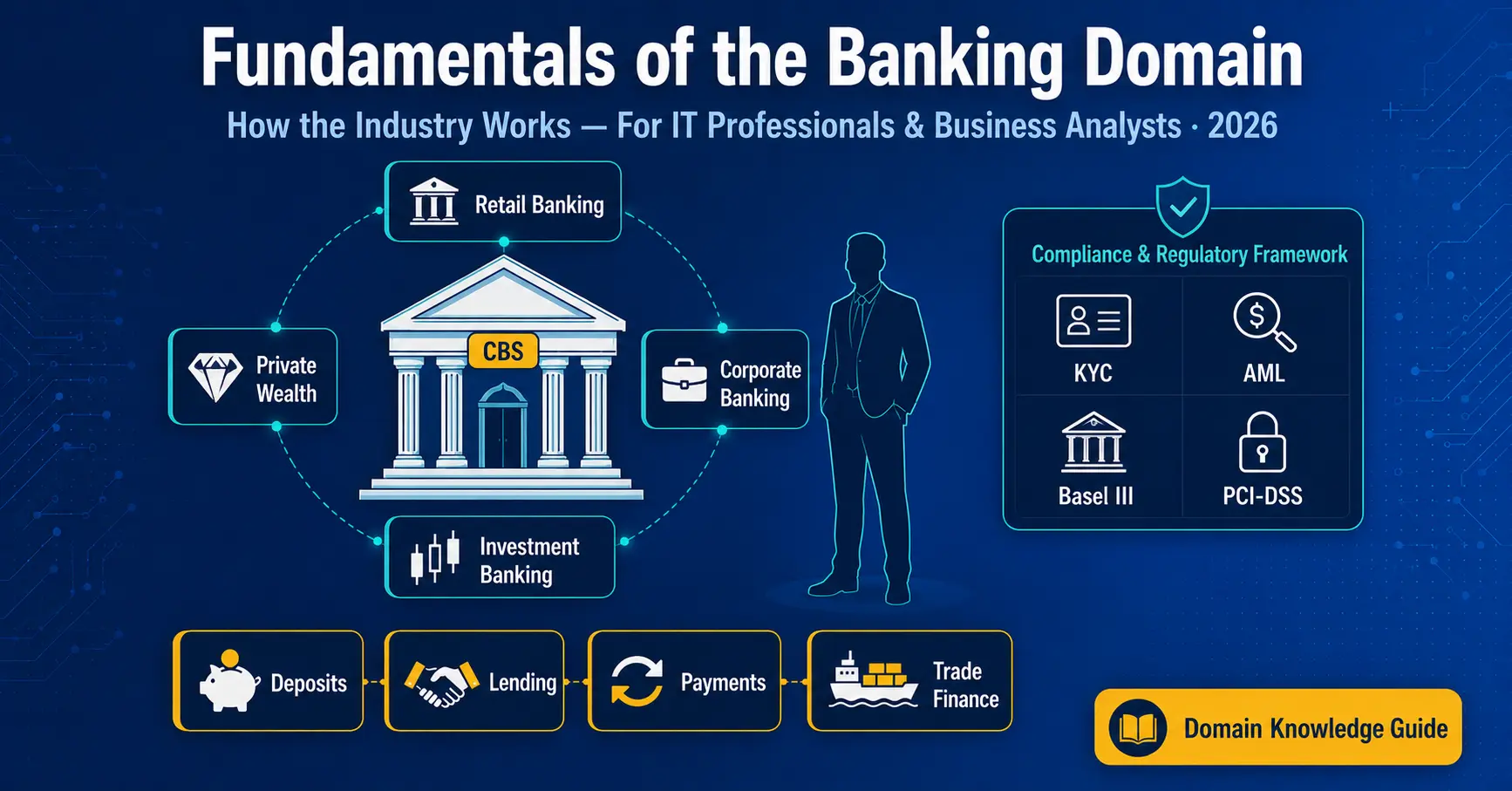

What Is the Banking Sector?

At its core, a bank has one simple function: take in money from those who have it and lend it to those who need it, earning a margin in between. Everything else (the regulations, the technology stacks, the products) exists to support, safeguard, and scale that fundamental exchange.

The banking sector forms the backbone of the BFSI domain (Banking, Financial Services, and Insurance). Globally, the banking sector employs tens of millions of people and spends over $700 billion annually on technology. In the US alone, the top four banks hold assets exceeding $10 trillion. Across the UK, Australia, Canada, and India, banking is consistently among the top three industries for IT investment, making it one of the most significant sources of work for IT professionals and Business Analysts worldwide.

Annual global banking IT spend

Technology investment across the banking sector worldwide, accelerating with digital transformation (IDC, 2024).

Assets held by top 4 US banks

JPMorgan Chase, Bank of America, Wells Fargo, and Citigroup, illustrating the scale of technology infrastructure needed.

Banks and credit institutions globally

Across the US, UK, EU, Australia, Canada, and Asia. Each has distinct products, regulations, and technology stacks.

Primary Banking Segments

Banks organise their operations into distinct business segments, each serving different customers with different products. Understanding which segment a project falls into determines the systems, processes, and regulatory constraints that matter most.

Retail Banking

Services targeted at individual consumers. This covers savings and checking accounts, personal loans, mortgages, and credit cards. It is the highest-volume segment and the one most end-users interact with daily. Technology projects here include digital account opening, mobile banking apps, and credit scoring.

Corporate and Wholesale Banking

Focused on businesses and institutions. Products include large-scale loans, trade finance, cash management, and syndicated lending. Transaction values are much higher than retail, though volumes are lower. IT projects here typically involve treasury systems, corporate portals, and trade finance platforms.

Investment Banking

Helps corporations and governments raise capital through underwriting (stocks and bonds), mergers and acquisitions (M&A), and advisory services. Investment banking operates in capital markets, requiring knowledge of financial instruments, deal structures, and market regulations. Systems here include front-office trading platforms and risk engines.

Private Banking and Wealth Management

Wealth management services provided to high-net-worth individuals (HNIs), covering personalised investment strategies, estate planning, and trust management. Projects in this segment involve portfolio management systems, advisory platforms, and regulatory suitability checks.

Why this matters for IT and BA work: The segment you are working in determines which CBS modules are in scope, which regulations apply, and which banking stakeholders you will be speaking with. A BA who confuses retail and corporate processes can miss critical requirements.

Core Banking Products and Services

Every banking IT project is ultimately about enabling, modifying, or reporting on a banking product. Understanding what each product is and how it works is essential before you can write requirements for it or test it meaningfully.

Deposits

Accounts where clients store money. Savings accounts pay interest and allow withdrawals. Checking (current) accounts are designed for frequent transactions. Fixed or term deposits lock money for a set period at a higher rate. Deposits are a bank’s primary funding source: the raw material it uses to make loans.

Credit and Lending

The other side of the balance sheet. Banks charge interest on credit products: mortgages, personal loans, auto loans, business loans, education loans, overdrafts, and credit cards, at rates above what they pay on deposits. The difference is the net interest margin (NIM), which drives most of a bank’s profitability. Interest is typically pegged to a benchmark rate set by the central bank.

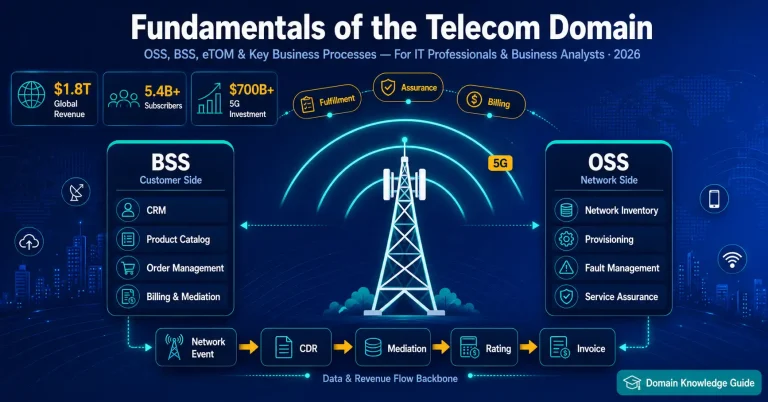

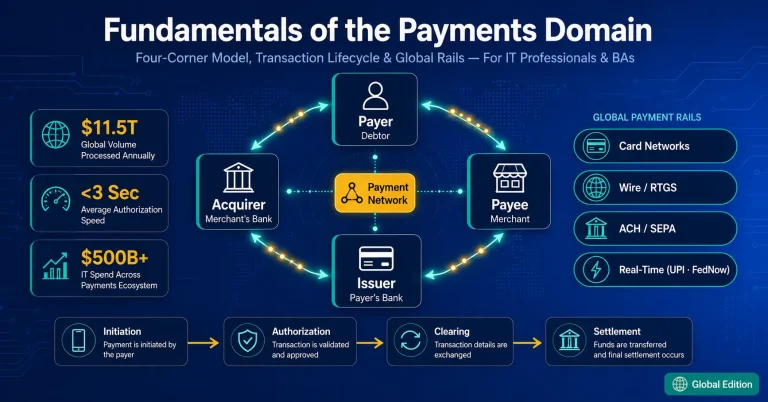

Payments and Remittance

Facilitating the movement of money across local and global networks. Payment rails vary by country but follow common patterns: real-time gross settlement (RTGS/Fedwire/CHAPS) for large-value transfers, batch clearing (ACH/BACS/NEFT) for retail payments, instant payment schemes (FPS/UPI/Zelle/PayID) for consumer transactions, and SWIFT for international transfers. Each channel has different processing rules, cut-off times, and integration requirements.

Trade Finance

Products that reduce risk in international trade. A Letter of Credit (LC) guarantees that a seller receives payment once shipment conditions are met. A bank guarantee commits the bank to cover a default. Banks also offer bill discounting and export finance. Trade finance is heavily document-intensive and SWIFT-dependent, making it a distinct and complex IT project area.

Deposits

Savings, current, fixed and recurring accounts: the bank’s funding base.

Credit and Lending

Mortgages, personal loans, business loans, cards: the bank’s primary revenue source.

Payments

RTGS, ACH, Faster Payments, SWIFT: domestic and cross-border fund movement across payment rails globally.

Trade Finance

Letters of Credit, bank guarantees, bill discounting for international commerce.

Banking Fundamentals for BAs and IT Professionals

Watch this structured lesson covering core banking transactions, ledgers, accounts clearing, and regulatory compliance standards, explained for IT and BA roles.

Watch Lesson NowRegulatory and Compliance Frameworks

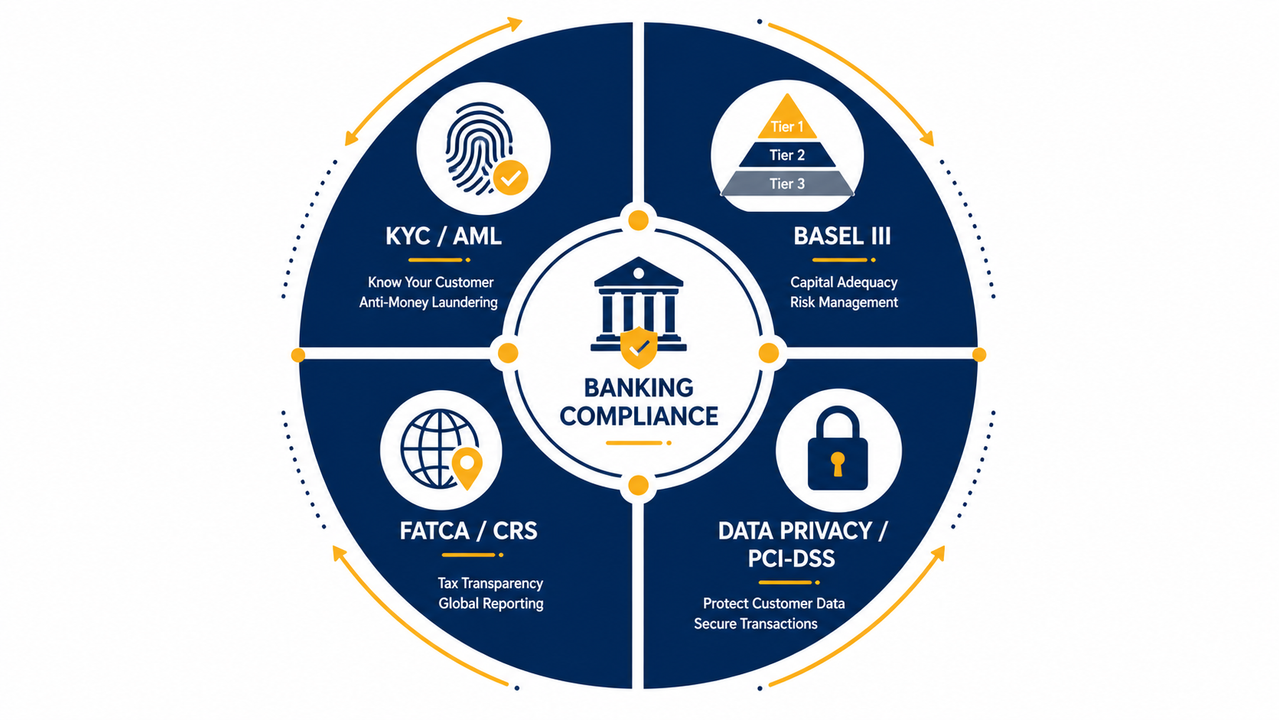

Banking is one of the most heavily regulated industries in the world, for good reason: banks hold public deposits and failure can cascade through the entire economy. For IT professionals, regulation is not background noise: a significant share of banking projects exist solely to meet regulatory requirements.

KYC (Know Your Customer) and CDD (Customer Due Diligence)

Before a bank can open an account or lend money, it must verify who the customer is and assess the risk they represent. This process: Know Your Customer, or KYC: involves collecting identity documents, verifying them against official records, and screening against sanctions and PEP (Politically Exposed Person) lists. Customer Due Diligence (CDD) goes further, assessing the source of funds and monitoring account behavior over time. Every bank has a digital KYC workflow, making this one of the most common BA project areas.

AML (Anti-Money Laundering)

Banks are legally required to detect and prevent their platforms from being used to move illicitly obtained money. AML rules require real-time transaction monitoring, generation of Suspicious Activity Reports (SARs) and Currency Transaction Reports (CTRs), and ongoing screening against watchlists. AML systems are complex and expensive: integrating with the CBS, payment systems, and external data sources simultaneously.

Basel Accords (Basel III / IV)

Global banking standards issued by the Basel Committee on Banking Supervision (BCBS) that regulate how much capital a bank must hold relative to its risk. The Capital to Risk-weighted Assets Ratio (CRAR) is the headline metric. Basel III also introduced liquidity ratios (LCR, NSFR). These rules drive a constant stream of regulatory reporting projects and risk system implementations.

Data Security and Privacy

Banks handle sensitive financial and personal data at massive scale. Standards like PCI-DSS govern payment card data globally. Regional data protection laws (GDPR in Europe, DPDP in India, the Privacy Act in Australia, PIPEDA in Canada, and state-level laws in the US) set rules on customer consent and data handling. FATCA and CRS require banks in most countries to report on foreign nationals’ accounts to tax authorities. Every technology system in a bank must be designed around these constraints.

Central Banks and Prudential Regulators

RBI (India), Federal Reserve/OCC (US), PRA (UK), APRA (Australia), OSFI (Canada): licensing, monetary policy, and supervisory rules for banks in each jurisdiction.

KYC / AML

Customer identity verification and transaction monitoring: mandatory for every bank account and product.

Basel III / IV

Capital adequacy (CRAR), liquidity standards, and risk-weighting norms from the Basel Committee.

Priority Sector Lending

Mandatory share of credit to agriculture, MSME, and weaker sections: drives reporting system projects.

FEMA and FATCA/CRS

Foreign exchange management and cross-border tax reporting obligations for banks with NRI or international accounts.

Data Protection Laws

GDPR (EU/UK), DPDP (India), Privacy Act (Australia), PIPEDA (Canada): consent, data handling, and customer privacy obligations.

Financial Instruments and Markets

Banks: especially investment and corporate banking divisions: work extensively with financial instruments traded in capital markets. IT and BA professionals working on treasury, trading, or risk management systems need to understand what these instruments are and how they behave.

Equities

Shares representing ownership in a company. Banks underwrite equity issuances (IPOs), manage equity portfolios for clients, and participate in secondary markets. Equity data flows are high-velocity and require real-time pricing systems.

Fixed Income

Bonds and debt securities paying fixed or variable interest. Government bonds (G-Secs), corporate bonds, and money market instruments. Banks hold G-Secs to meet SLR requirements. Fixed income trading involves complex yield calculations and settlement rules.

Derivatives

Financial contracts: futures, options, swaps: whose value is derived from an underlying asset such as a currency, interest rate, or commodity. Banks use derivatives to hedge risk and for client hedging solutions. Derivatives systems require sophisticated valuation and risk engines.

Beyond these three, banks also deal in foreign exchange (forex spot, forward, and swap markets), commodities (for trade finance clients), and structured products. Each instrument class has its own settlement cycle, pricing methodology, and regulatory reporting requirement.

How Banks Operate Day-to-Day

Understanding the operational machinery of a bank is where IT and BA professionals get the most practical value. Three areas come up on almost every project:

Core Banking Systems (CBS)

The centralised backend that allows banks to process daily transactions and update accounts in real time. Finacle, FLEXCUBE, Temenos Transact, and BaNCS are widely deployed across Asia-Pacific, the Middle East, and Africa. Finastra, FIS, and Fiserv dominate North America and Europe. All channels (branch, ATM, internet, mobile) connect to the CBS for account updates.

Payments and Clearing

Mechanisms for transferring funds between parties: wire transfers, digital wallets (UPI), automated clearing houses (NACH), and real-time gross settlement (RTGS). Each payment rail has different settlement cycles and failure handling rules: critical for BA requirements work.

Risk Management and Compliance

Ensuring adherence to Basel III frameworks and jurisdiction-specific regulators (Federal Reserve, PRA, APRA, RBI) to manage credit, liquidity, and operational risk while preventing financial fraud. This includes NPA monitoring, capital adequacy reporting, and AML transaction screening: all requiring dedicated technology systems.

Build the banking knowledge that gets you staffed on projects

Techcanvass’s Banking Training covers the complete banking lifecycle, products, core systems, and regulatory landscape: built specifically for IT professionals and Business Analysts, with real project scenarios.

Core Banking Systems: A Closer Look

A Core Banking System is the central platform managing a bank’s primary operations: accounts, deposits, loans, transactions, and interest calculations: in real time across all channels. CBS is where almost every banking IT project starts and ends.

Major CBS platforms globally

| Platform | Vendor | Where you’ll see it | Typical project types |

|---|---|---|---|

| Finacle | Infosys | Widely deployed across India, Middle East, Africa, and Southeast Asia | Implementation, upgrade, digital and API banking integration |

| FLEXCUBE | Oracle (OFSS) | Strong in India, Southeast Asia, and globally through Oracle’s banking customer base | Implementation, custom module development, regulatory reporting |

| Temenos Transact | Temenos | Significant in Europe, North America, Middle East, and Asia-Pacific | T24 to Transact migration, cloud deployment |

| BaNCS | TCS Financial Solutions | Used across Asia, Europe, and international banking subsidiaries | Implementation, payments module, trade finance |

| FinnOne Neo | Nucleus Software | Dominant in India’s NBFC sector; used across South and Southeast Asia for lending | LMS implementation, co-lending, collections module |

| Finastra / FIS / Fiserv | Finastra, FIS, Fiserv | Dominant in North America, UK, and Australia: the primary CBS vendors for US and Canadian banks | Core banking modernisation, digital banking, open banking API platforms |

Key CBS modules a BA needs to know

| Module | What it manages | BA focus areas |

|---|---|---|

| CIF (Customer Information File) | Single master customer record across all products | Customer 360, deduplication, KYC linkage, data migration |

| Deposits / CASA | Savings, current, fixed and recurring accounts | Product configuration, interest rules, statement generation |

| Loans and Advances | Loan accounts, EMI schedules, NPA classification | Repayment logic, prepayment, restructuring, provisioning |

| Payments | NEFT, RTGS, IMPS, UPI, internal transfers | Channel integration, limits, cut-off times, reconciliation |

| General Ledger (GL) | All accounting entries: the bank’s financial backbone | GL mapping, EOD/SOD batch, financial reporting |

The Lending Lifecycle

Lending is the primary revenue-generating activity of banks and one of the most project-intensive areas of banking IT. Every stage of the loan lifecycle: from application to recovery: has a corresponding system and a set of business rules a BA must understand.

| Stage | What happens | Systems involved |

|---|---|---|

| 1. Application | Customer applies via branch, digital app, or DSA | LOS: application capture, document upload, lead management |

| 2. Credit Assessment | Income verification, credit bureau check (CIBIL/Equifax/Experian), collateral valuation, risk scoring | Bureau integration, credit scoring engine, appraisal tools |

| 3. Sanction | Credit committee approves amount, rate, tenure, conditions | LOS approval workflow, sanction letter generation |

| 4. Documentation | Loan agreement, mortgage deed, hypothecation executed | Document Management System, eSign integration |

| 5. Disbursement | Loan amount credited or paid to third party | CBS disbursement module, reconciliation |

| 6. Servicing | EMI collection, prepayment, rate changes, statements | Loan Management System (LMS) |

| 7. Collections | Reminders, NPA classification, SARFAESI, recovery | Collections system, NPA module |

Essential lending terms: LTV (Loan-to-Value), EMI, NPA (Non-Performing Asset), GNPA/NNPA, PCR (Provision Coverage Ratio), credit score (CIBIL/FICO/Equifax), DPD (Days Past Due), secured loan recovery laws (SARFAESI/UCC), and mandatory lending targets (Priority Sector/CRA requirements).

What IT Professionals and Business Analysts Need to Know

Banking is one of the most complex and rewarding domains for IT and BA professionals. Every product is a legally binding contract subject to regulatory oversight, and every system change has compliance implications. Here is where knowing this sector pays off in practice:

| Activity | Without sector knowledge | With sector knowledge |

|---|---|---|

| Requirements elicitation | Misses critical rules: interest methods, NPA provisioning, return formats | Asks precise questions about product config, processing rules, and regulatory impact |

| User story writing | Generic stories miss scenarios: premature closure penalty, dormant account, lien marking | Complete stories with banking-accurate acceptance criteria and edge cases |

| Stakeholder communication | Needs every term explained: CASA, NPA, credit bureau scores, Basel III | Speaks confidently with branch, credit, compliance, and treasury teams |

| Gap analysis | Cannot distinguish CBS configuration limits from actual requirement gaps | Maps requirements to CBS capability and identifies config vs development gaps clearly |

Common projects IT and BA professionals work on

- CBS Implementation or Migration: moving to a new core banking platform; the largest and most complex banking IT project.

- Digital Banking Platform: retail internet banking, mobile app, corporate banking portal.

- Loan Origination System (LOS): end-to-end digital loan application and sanction workflow.

- KYC and AML System: customer due diligence, transaction monitoring, STR and CTR reporting.

- Regulatory Reporting: RBI returns, CRILC, Basel III capital adequacy, FATCA and CRS.

- Payment Hub: centralising domestic payment rails (RTGS, ACH, Faster Payments, UPI) and SWIFT into one orchestration layer.

- Open Banking and API Banking: account aggregator integrations and fintech API gateways.

Key Banking Terms Explained

Stakeholders in banking expect you to know the vocabulary. These are the terms that come up most often in project discussions.

Accounts and Deposits

CASA

Current Account and Savings Account: a bank’s low-cost deposits, used as a measure of funding quality.

CIF

Customer Information File: the single master record linking all products a customer holds.

KYC

Know Your Customer: mandatory identity verification before account opening or lending.

Routing / Sort Codes

IFSC (India), ABA routing number (US), Sort Code (UK), BSB (Australia): codes that identify a bank branch for fund transfer routing.

Lending and Risk

NPA

Non-Performing Asset: a loan where repayment has stopped; the central measure of asset quality.

LTV

Loan-to-Value: the loan amount as a percentage of the asset used as collateral.

DPD

Days Past Due: how long a payment obligation has been overdue.

Secured Loan Recovery Laws

SARFAESI (India), UCC Article 9 (US), LPA 1925 (UK): frameworks allowing banks to recover secured loans, often without full court proceedings.

Regulatory and Treasury

Reserve Requirements

Mandatory liquidity and capital buffers set by central banks: CRR/SLR (India), reserve ratios (US Fed), liquidity coverage ratio (LCR) under Basel III globally.

CRAR

Capital to Risk-weighted Assets Ratio: the Basel measure of a bank’s capital adequacy.

NIM

Net Interest Margin: the difference between interest earned on loans and interest paid on deposits.

Nostro / Vostro

Correspondent banking accounts used for settling international forex transactions between banks.

How to Build Your Banking Knowledge

You do not need a finance degree. A structured, project-oriented approach: starting with the business model before moving to systems and regulations: works best for IT professionals and BAs.

Start with how banks make money

Understand the deposit-lending spread and the interest margin before diving into products or systems. Everything else flows from this.

Learn the segments and products

Understand what retail vs corporate banking means, and how deposits, lending, payments, and trade finance each work operationally.

Map products to technology systems

Know what a CBS does and how its modules correspond to banking functions. Then add LOS, LMS, and payment hubs.

Learn the regulatory landscape

KYC/AML, Basel III, and the regulatory framework relevant to your target market (Fed/OCC, PRA, APRA, RBI): understand what each requires and which IT systems it touches.

Take a structured course

A focused banking training program teaches terminology, processes, systems, and regulations in the right sequence: and with real project examples.

Ready to specialise in BFSI?

Explore Techcanvass’s domain guides and structured training for IT professionals and Business Analysts who want to win banking and BFSI projects with confidence.

Frequently Asked Questions

What is the banking domain?

What does banking domain knowledge mean for an IT professional?

What are the four primary banking segments?

What is a Core Banking System (CBS)?

Why is regulatory knowledge important for banking IT projects?

How can someone build banking knowledge without a banking background?

Explore the Full BFSI Domain

Banking sits within the broader BFSI sector. These guides connect the full picture for IT professionals and Business Analysts working across the industry.

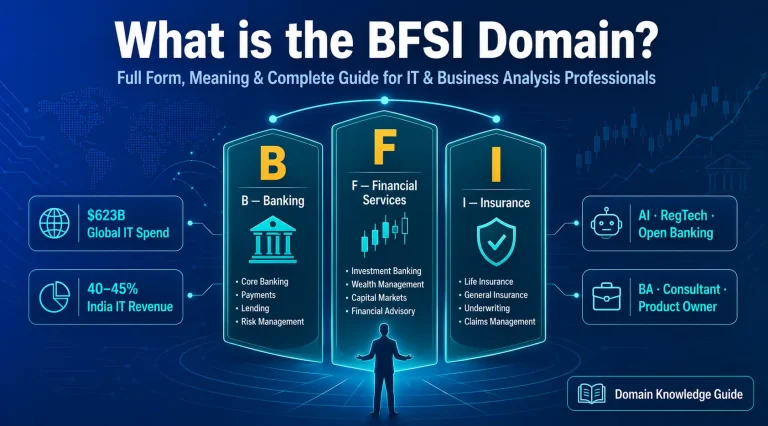

What is the BFSI Domain? Full Form, Meaning and Complete Guide

The parent sector explained: how banking, financial services, and insurance connect, and what IT professionals need to know about each.

Read guide PaymentsPayments Domain Knowledge: A Complete Guide

How domestic and cross-border payment rails work: RTGS, ACH, Faster Payments, SWIFT, card networks, and what BA and IT professionals need to know globally.

Read guide Capital MarketsInvestment Banking Domain Knowledge

Equities, fixed income, derivatives, M&A, and capital markets operations: for professionals working on front-office or trading technology.

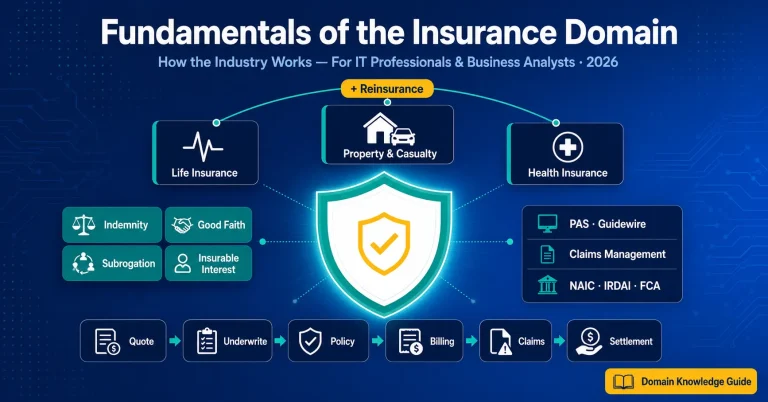

Read guide InsuranceInsurance Domain Knowledge: A Complete Guide

Life, health, and general insurance products, underwriting, claims, and the core systems: for IT and BA professionals in the insurance vertical.

Read guide Career GuidanceWhich BA Domain Should You Choose? Banking, Insurance, or Healthcare?

A structured comparison to help IT professionals and BAs decide where to build their domain expertise.

Read guide TrainingBanking Domain Training for IT and BA Professionals

A structured program covering banking products, processes, CBS systems, and regulatory frameworks: with real project scenarios.

View training