Fundamentals of the

Payments Domain: How the Industry Works

Understand the global infrastructure moving digital money. From the four-corner model and transaction lifecycles to core systems like gateways, processors, and modern messaging standards. Built for IT professionals and Business Analysts.

What exactly is the payments industry?

This sector covers the complete ecosystem responsible for moving funds between individuals, businesses, and financial institutions. It encompasses the underlying rails (like ACH, SWIFT, or real-time networks), the institutions holding the funds, and the technology that securely routes the data.

For IT and Business Analysis professionals, mastering this area means understanding the exact mechanisms behind how a transaction starts at a checkout screen and successfully settles in a bank account days later.

Core Focus Areas

- 1Participants (Issuers, Acquirers)

- 2Transaction Flow (Auth to Settlement)

- 3Back-End Technology (Gateways, Switches)

Elements of Payments Domain

Working on financial technology projects requires specific knowledge of how the industry operates. The elements of this sector are defined by high-speed data exchanges, strict regulatory oversight, and complex integrations between legacy banking cores and modern digital interfaces.

Professionals in this space must understand more than just code or basic requirements. You need working knowledge of standard data formats, the difference between messaging vs. actual settlement, and the financial risks involved when a system fails.

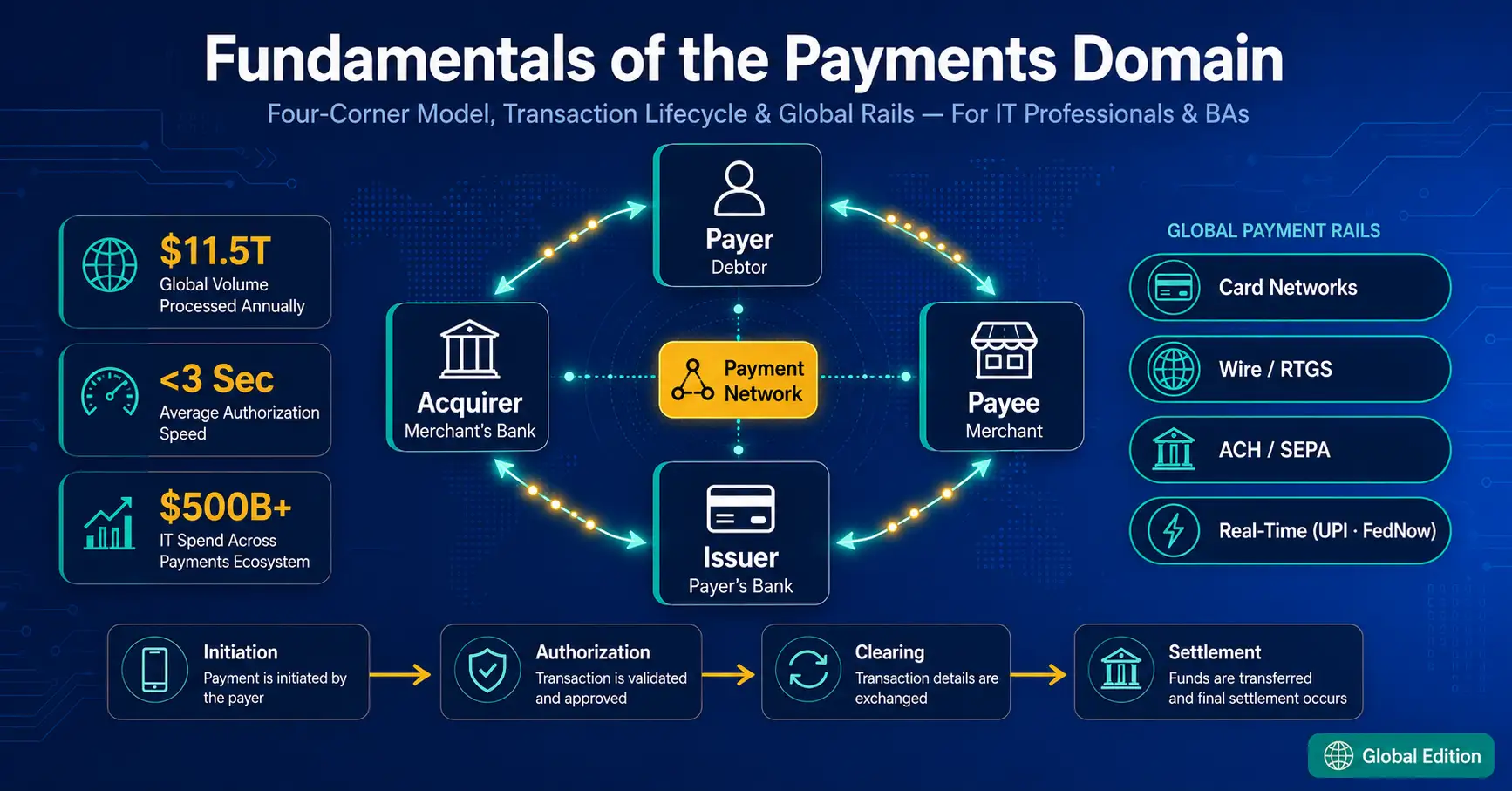

Global Volume

Estimated digital transaction value worldwide.

Auth Speed

Average time a card network takes to approve a charge.

IT Spend

Annual global investment in financial infrastructure.

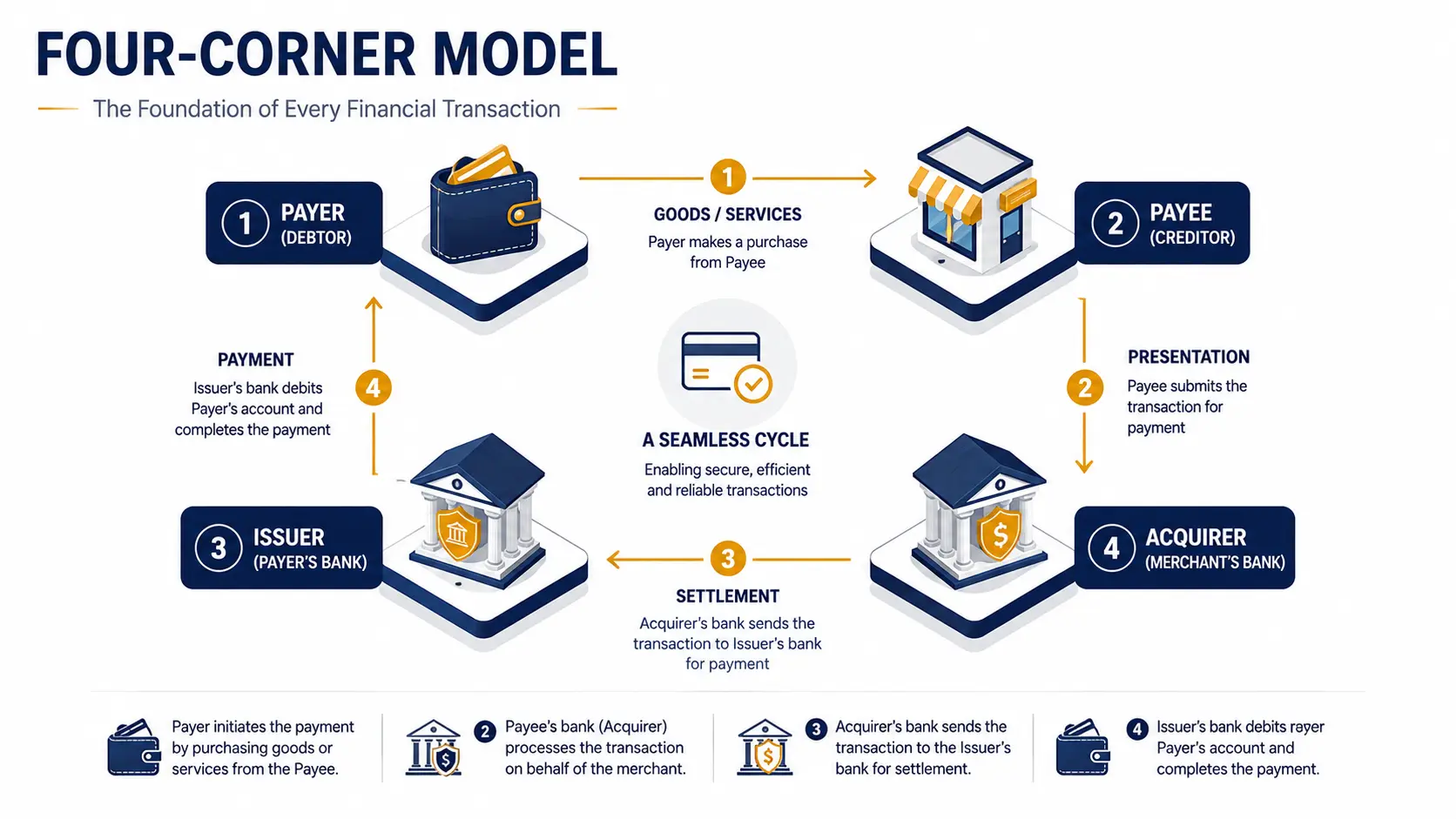

Key Stakeholders (The Four-Corner Model)

Virtually all modern transaction networks operate on a framework known as the Four-Corner Model. Understanding this structure is the absolute foundation for anyone documenting requirements or building financial software.

| Stakeholder | Definition | Role in IT Systems |

|---|---|---|

| 1. Payer (Debtor) | The individual or business sending the money. | User interface interaction, authentication (biometrics, passwords). |

| 2. Payee (Creditor) | The entity or merchant receiving the funds. | Point-of-Sale (POS) systems, checkout integrations. |

| 3. Issuer | The bank holding the Payer's funds. Approves or declines the transaction. | Core banking system checks, fraud scoring engines, account limits. |

| 4. Acquirer | The bank holding the Payee's account. Processes the payment on their behalf. | Merchant onboarding, risk management, batch settlement processing. |

Connecting these four corners are the Payment Networks and Gateways. These act as the secure data highways that transmit the requests between the Issuer and the Acquirer (e.g., Visa, Mastercard, or local networks).

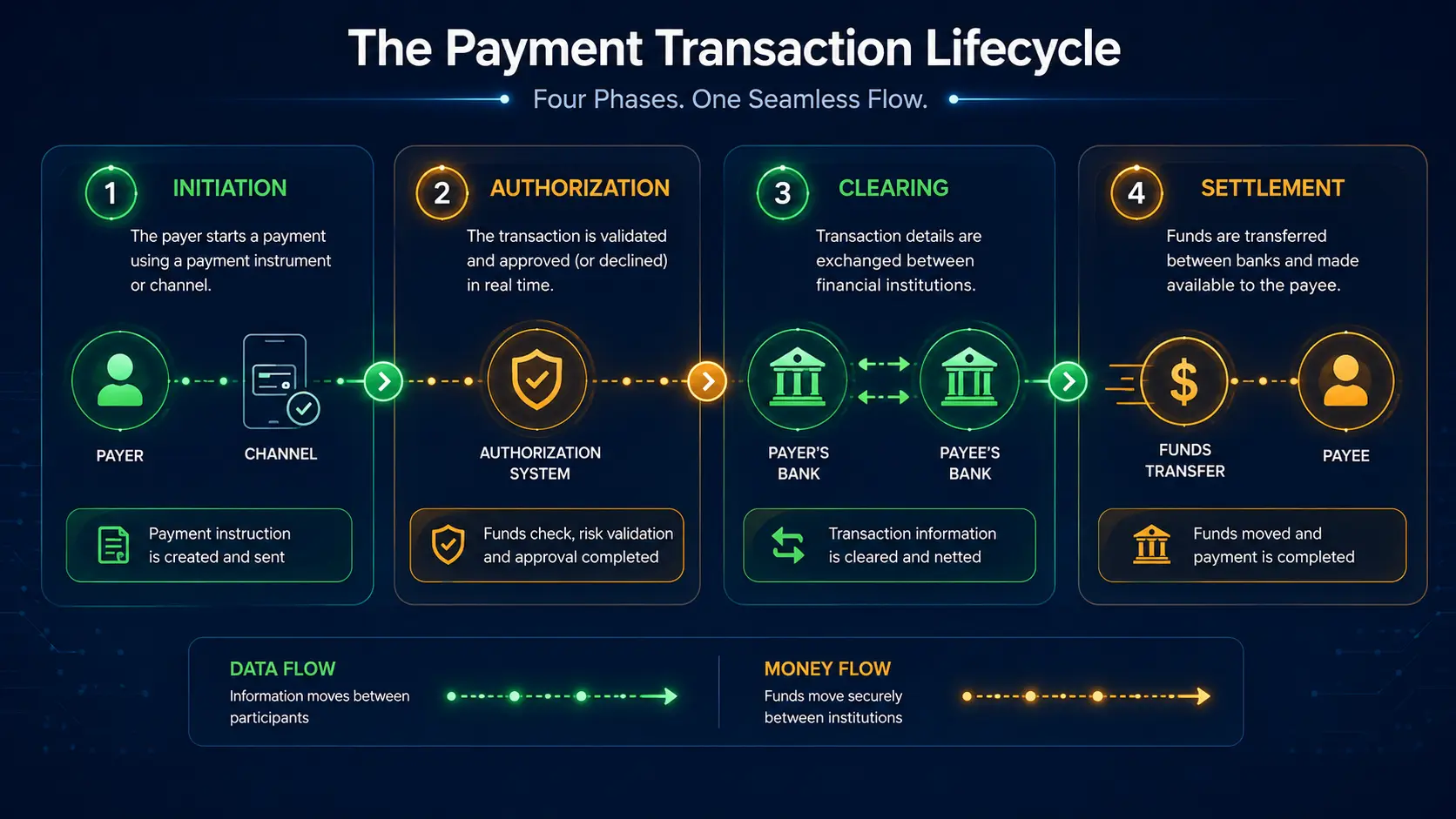

Transaction Lifecycle Phases

A digital purchase is not a single event. It is a sequence of distinct phases that happen across different timeframes. Confusing authorization with settlement is a common error that can ruin software logic.

Initiation

The payer provides their details. This could involve scanning a QR code, entering card data into an e-commerce checkout, or swiping at a terminal.

Authorization (Real-Time)

The request routes through the network to the issuer. The issuer verifies the account status, checks for sufficient funds, runs fraud checks, and immediately returns an "Approve" or "Decline" message.

Clearing (End of Day)

The exchange of final transaction data between the acquirer and issuer. The network calculates the exact financial obligations, including any interchange fees, before money actually moves.

Settlement (T+1 to T+2)

The actual transfer of funds from the issuer's bank to the acquirer's bank to finalize the purchase. While real-time systems settle instantly, traditional cards usually settle one or two business days later.

Master Financial Infrastructure Integration

Techcanvass's specialized training programs cover the end-to-end processing flows, global rail systems, and regulatory requirements you need to know to excel in IT projects.

Payment Types & Infrastructure

Different types of transactions require entirely different infrastructures, often referred to as "rails". Designing software for a payroll batch requires a different approach than building a real-time peer-to-peer transfer feature.

Card Networks

Credit, debit, and prepaid models running on centralized, global rails (Visa, Mastercard, Amex).

Wire Transfers (RTGS)

High-value, immediate, and irrevocable transfers between banks (e.g., Fedwire in the US, CHAPS in the UK).

Batch Processing (ACH / SEPA)

Systems built for volume over speed. Used globally for direct debits, payrolls, and low-value transfers processed in grouped files.

Real-Time Payments (RTP)

Modern infrastructure allowing instant account-to-account (A2A) transfers 24/7. Examples include FedNow (USA), UPI (India), and NPP (Australia).

Back-End Systems Explained

Behind the customer-facing apps lies a massive ecosystem of specialized software engines. IT teams must understand where these systems sit within the architecture.

| System Type | Primary Function | Examples / Context |

|---|---|---|

| Payment Gateways | Secure front-end tools that encrypt and transmit data securely from the merchant to the acquiring bank. | Stripe, Adyen, Braintree. Focuses heavily on API integration and checkout UX. |

| Payment Processors / Switches | The back-end engines that manage the heavy lifting: routing messages between merchants, acquirers, and card networks. | Fiserv, FIS, ACI Worldwide. Operates at massive scale and high availability. |

| Payment Hubs | Internal banking IT systems that centralize routing. They decide whether to send a transaction via Wire, ACH, or RTP. | Crucial for straight-through processing (STP) and format conversions inside large banks. |

| Card Management Systems (CMS) | Handles the complete lifecycle of a card product, from physical plastic issuance to credit limits and billing cycles. | TSYS. Vital for consumer banking operations. |

Global Messaging Standards

Institutions cannot communicate if they don't speak the same digital language. Understanding data schemas is a core requirement for developers and analysts.

ISO 20022

The modern, universal messaging standard adopted globally. It replaces legacy fixed-width formats with flexible XML/JSON data, providing richer, structured, and more transparent data across borders. It is the foundation for modern RTP systems.

SWIFT

A global messaging network used by thousands of institutions to securely transmit instructions for cross-border wires. Note that SWIFT itself does not move money; it only sends the secure messages authorizing the movement between correspondent banks.

The Role of Business Analysts in this Sector

Because financial transactions are heavily regulated and carry immediate financial consequences for failure, the role of a Business Analyst (BA) is highly specialized.

| Requirement Area | Why Domain Context Matters |

|---|---|

| Exception Handling | A BA must write stories for edge cases: What happens if authorization succeeds but settlement fails? How are partial refunds processed? How are chargebacks initiated? |

| System Mapping | Knowing exactly which system owns the logic. Should a fraud rule be placed at the gateway level or deep inside the issuer's core processing engine? |

| Data Fields | Understanding the difference between a BIN (Bank Identification Number) and a PAN, and knowing which fields are mandatory in an ISO 20022 message payload. |

Career Tip: Professionals who can fluently translate business needs into technical routing logic, while keeping compliance in check, are among the most sought-after profiles in the IT industry globally.

Regulatory Landscape

Every digital feature implemented in this industry has a compliance implication. Teams must design software with these global and regional frameworks built-in from day one.

PCI DSS (Global)

The global security standard requiring strict network architecture, encryption, and auditing for any system that stores or transmits cardholder data.

PSD2 & Open Banking (Europe/UK)

Mandates Strong Customer Authentication (SCA) and requires banks to open their infrastructure to third-party providers via secure APIs.

Data Privacy (GDPR, CCPA)

Strict rules around data minimization and user consent. Storing transaction histories requires careful masking and data retention policies.

Advance Your BA Career

Techcanvass offers structured learning paths to help you master complex industry sectors. Get the expertise needed to lead enterprise-scale software implementations.